Financial Wisdom

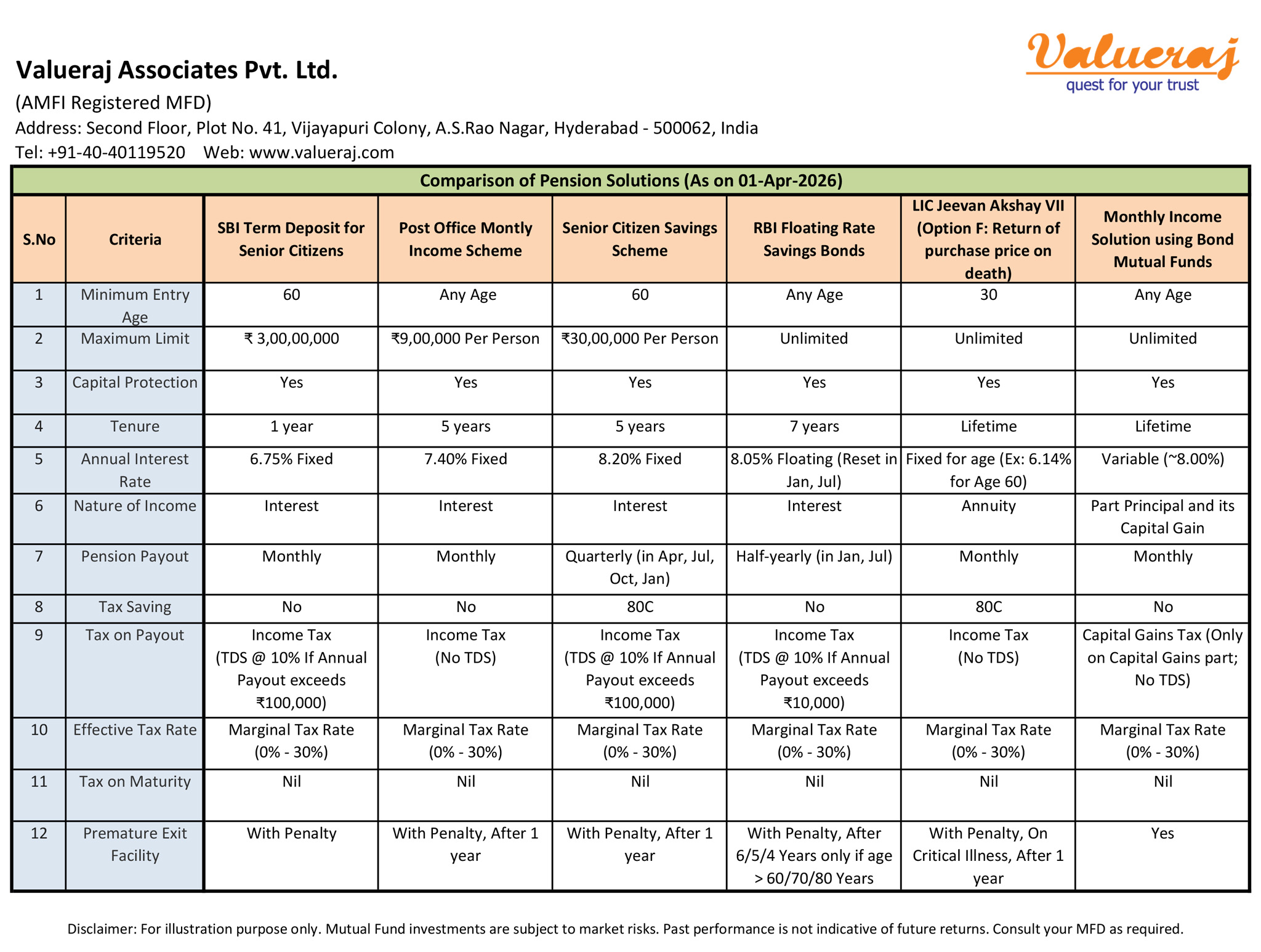

For senior citizens, there are several pension solutions available such as bank fixed deposits, post office schemes, govt pension schemes, annuity plans.However, very few know that bond mutual funds offer a better alternative solution with superior returns at lower tax liability.

Find below various pension solutions available vis-a-vis solution with bond mutual funds.

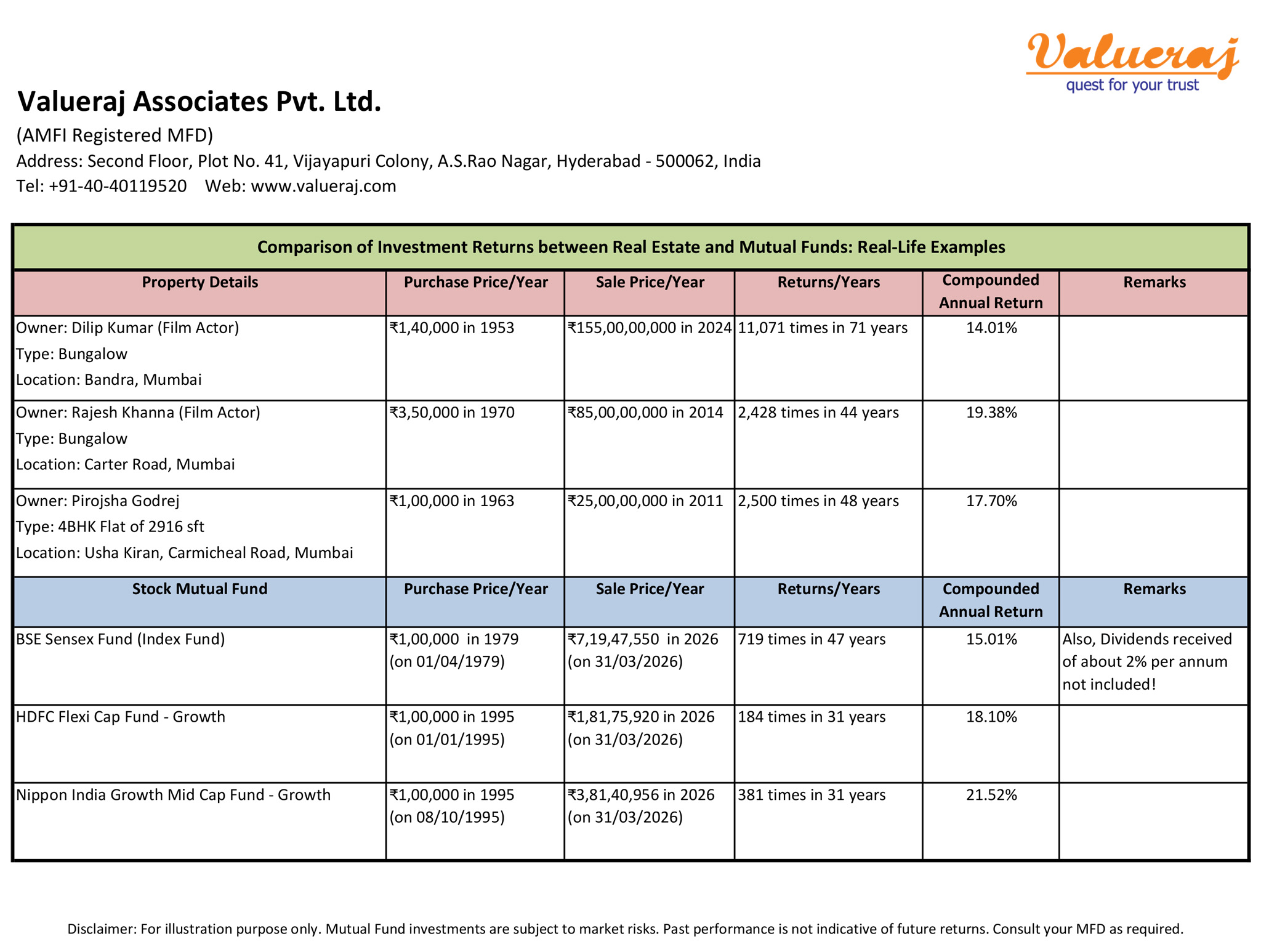

For wealth creation, many investors opt for investing only into real estate assets assuming that the returns would be superior to any other investments. However, historic data indicates that equity mutual funds have offered similar or better returns compared to real estate investments. Hence, it is wise to be invested in financial assets such as equity mutual funds too for better liquidity and diversification.

Find below some interesting real-life examples on returns of premier properties and select equity mutual funds.

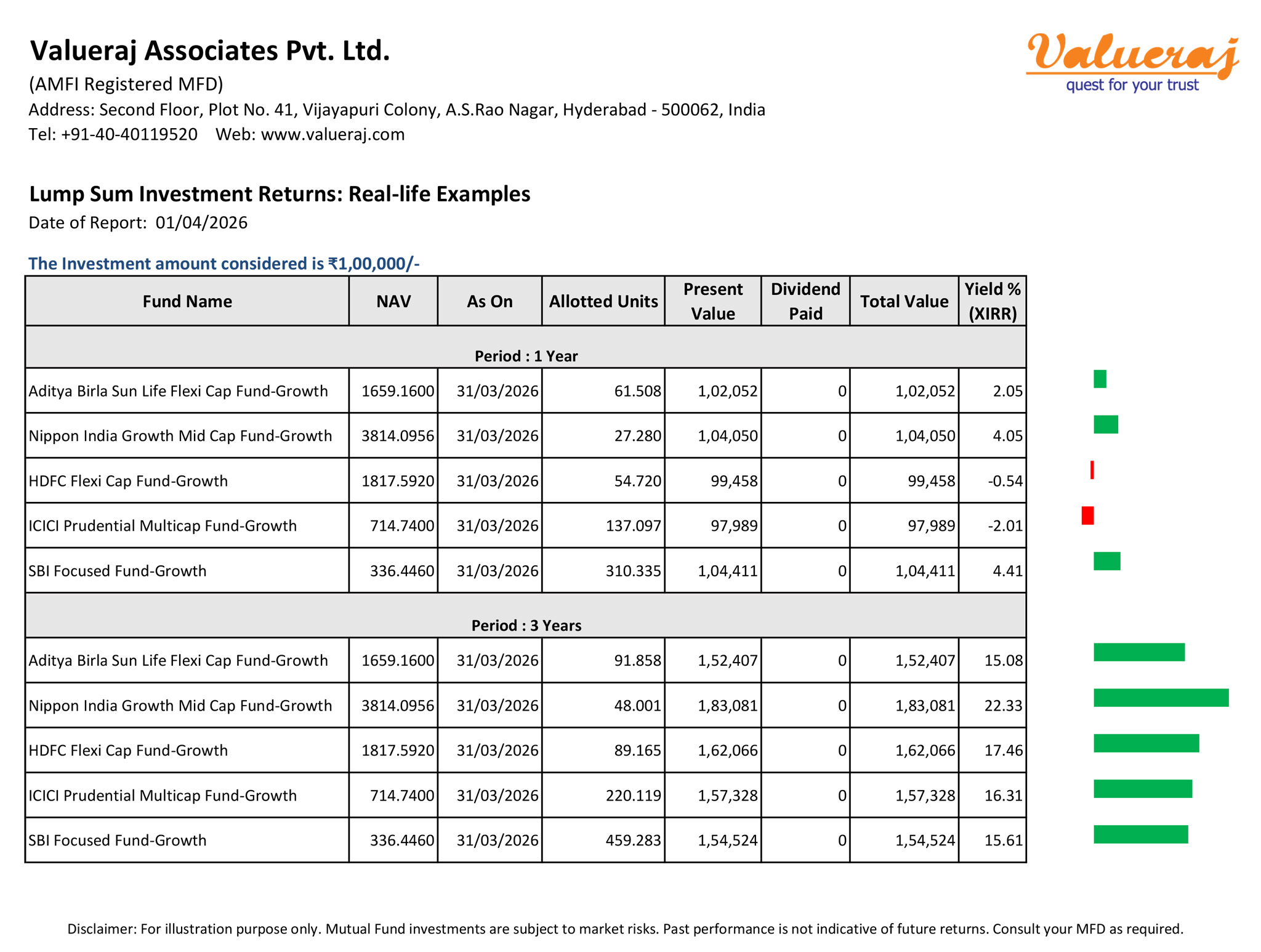

For wealth creation, it is always necessary to be invested in financial assets with inflation-beating returns. Equity mutual funds offer us a right choice in this regard, as they generate better post-inflation returns in the long-term.

Find below the real-life returns of lump sum investments in various equity mutual funds for different tenures.

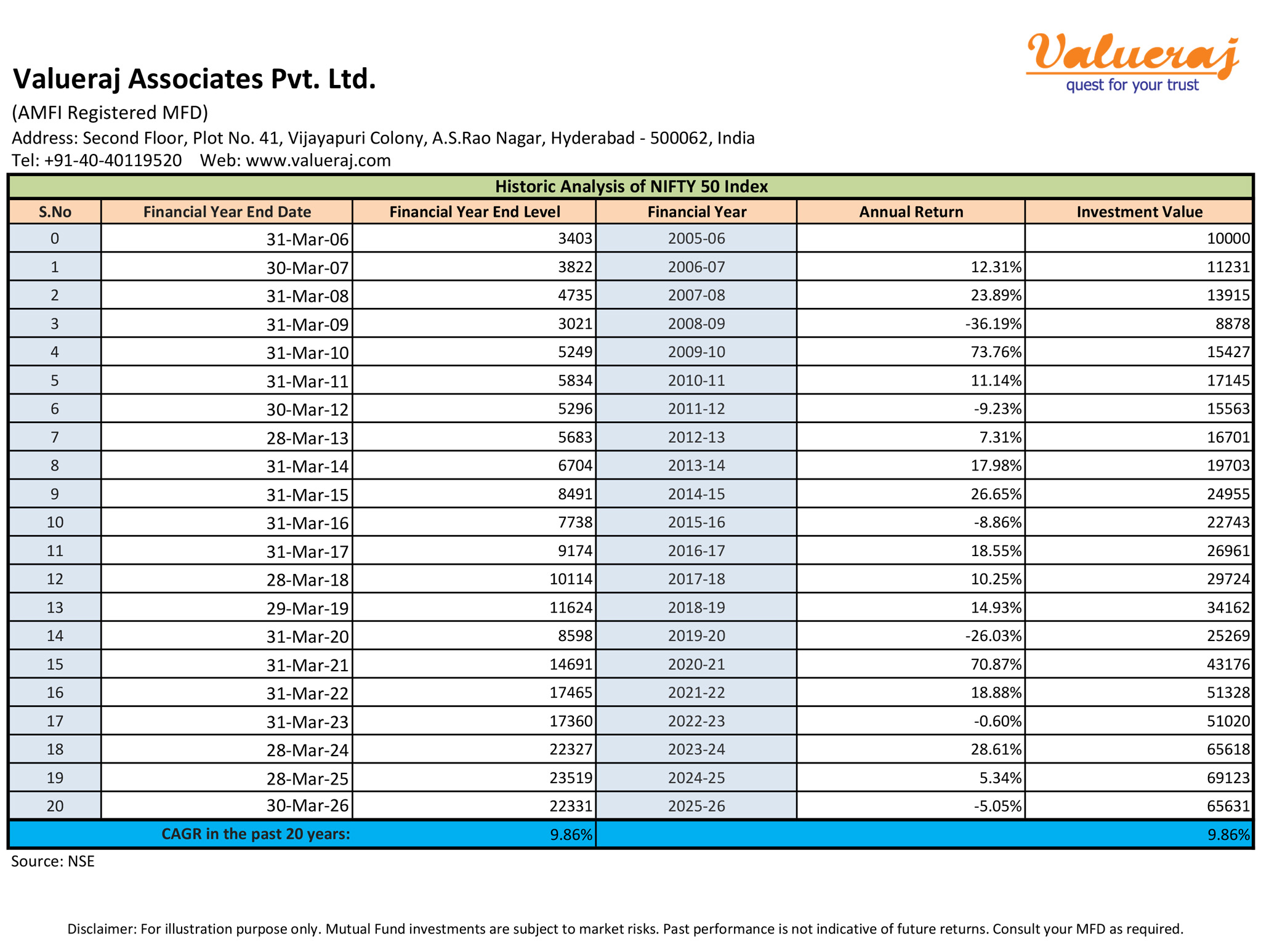

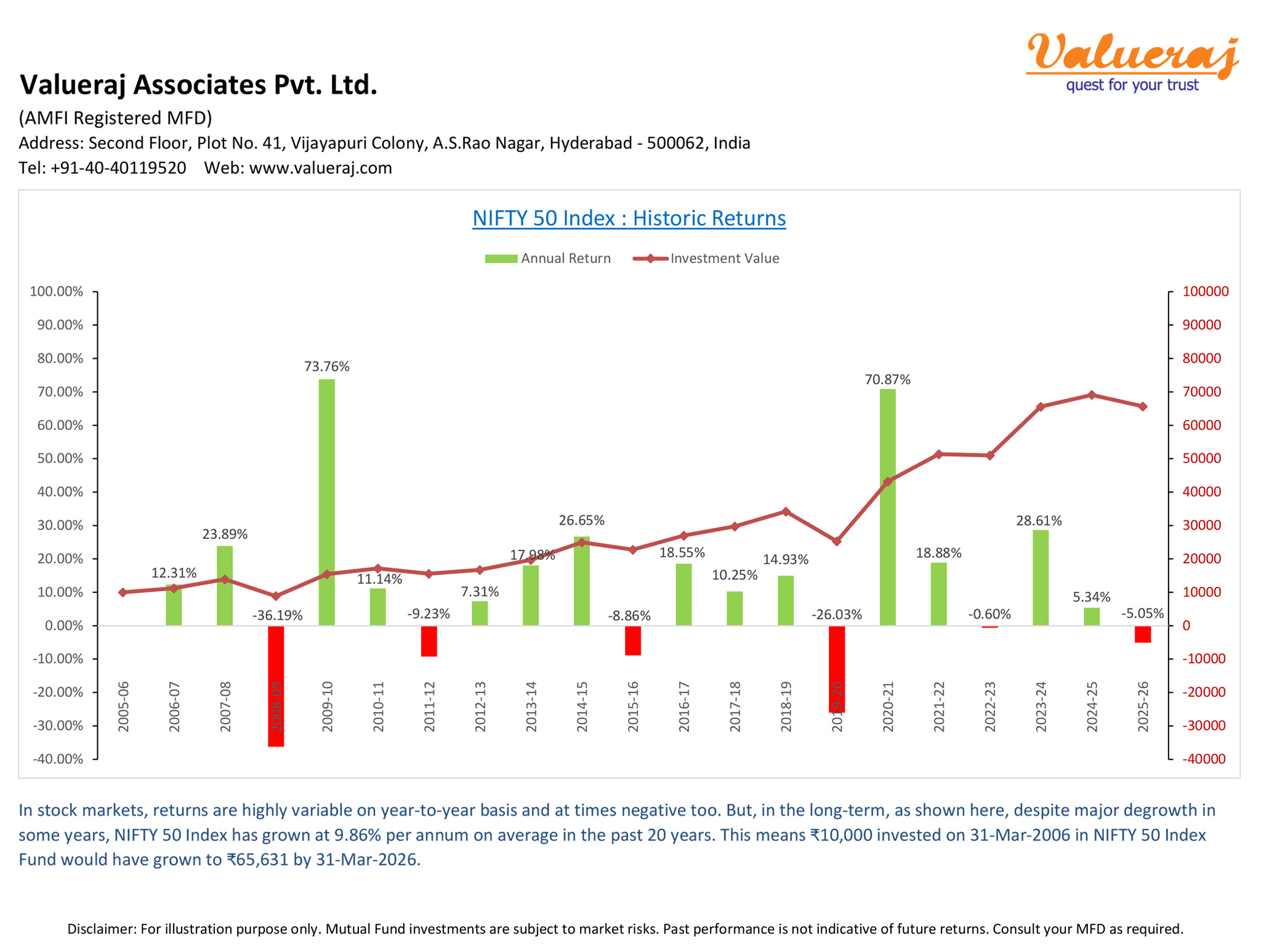

History has proved that stock market returns are highly volatile in the short-term. However, staying invested in stock markets for long-term can definitely be rewarding for investors.

Find below the historic returns of Nifty50 over last 20 years.

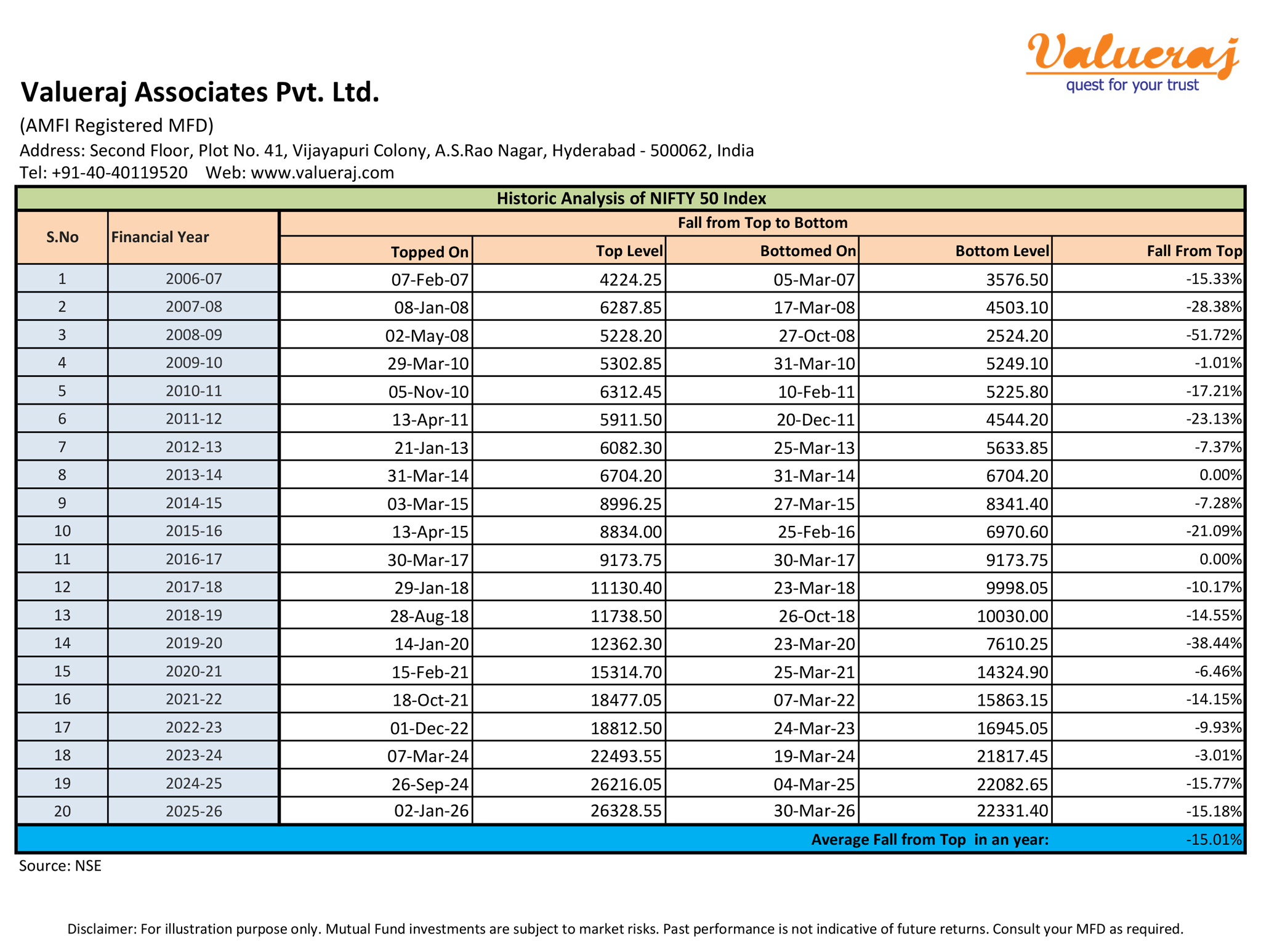

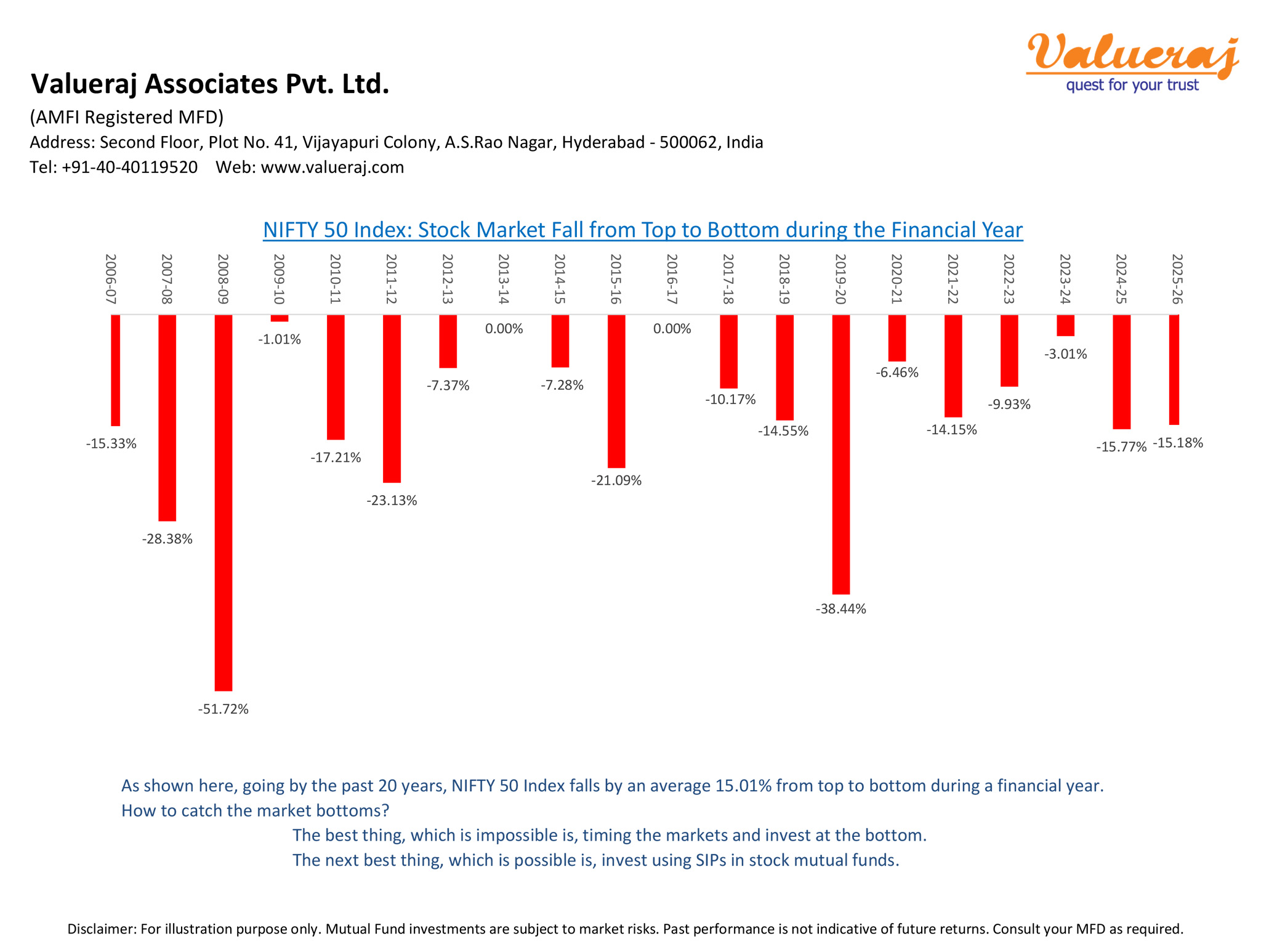

Stock markets always tend to be volatile and never predictable. They go through ups/downs depending on the levels of optimism/pessimism in investors.Therefore, deep corrections are common in any year and SIPs in equity mutual funds are the right means to catch these bottoms.

Find below the Nifty50 index fall from peak in each financial year in the past 20 years.

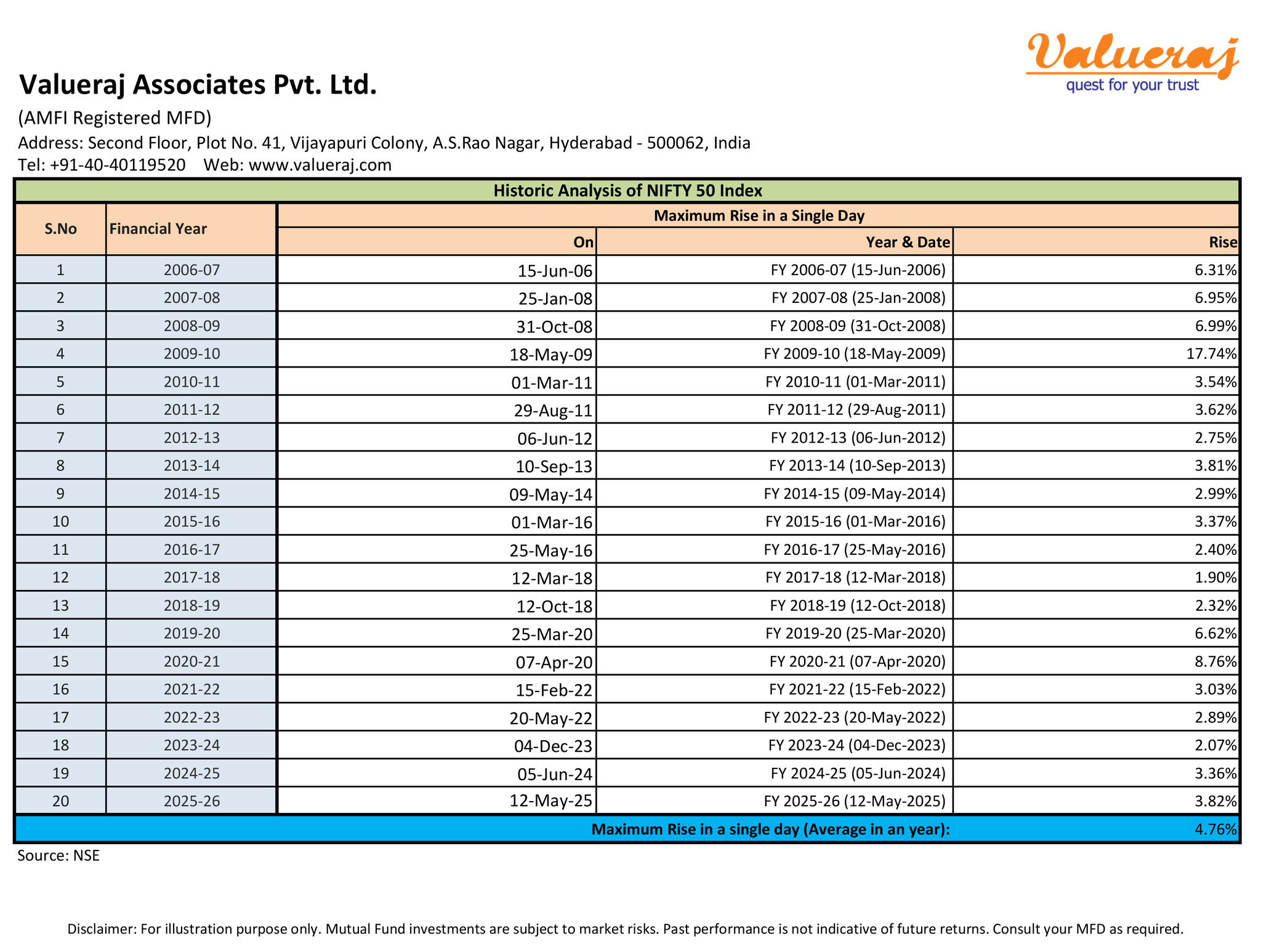

Stock markets never grow linearly. There can be sudden rises in a single day at times. Staying invested in stock mutual funds is the only way to catch these rises, rather than attempting to time the market.

Find below the maximum rise of Nifty50 index in a single day, in each financial year in the past 20 years.

Time waits for none, neither do our financial goals. The recent pandemic has taught all of us many lessons on how situations can become vulnerable unexpectedly.

Hence it is mandatory for all of us to have a clear conviction on savings and build a proper portfolio of financial products. A systematic and scientific process to achieve this is “Financial Planning”.

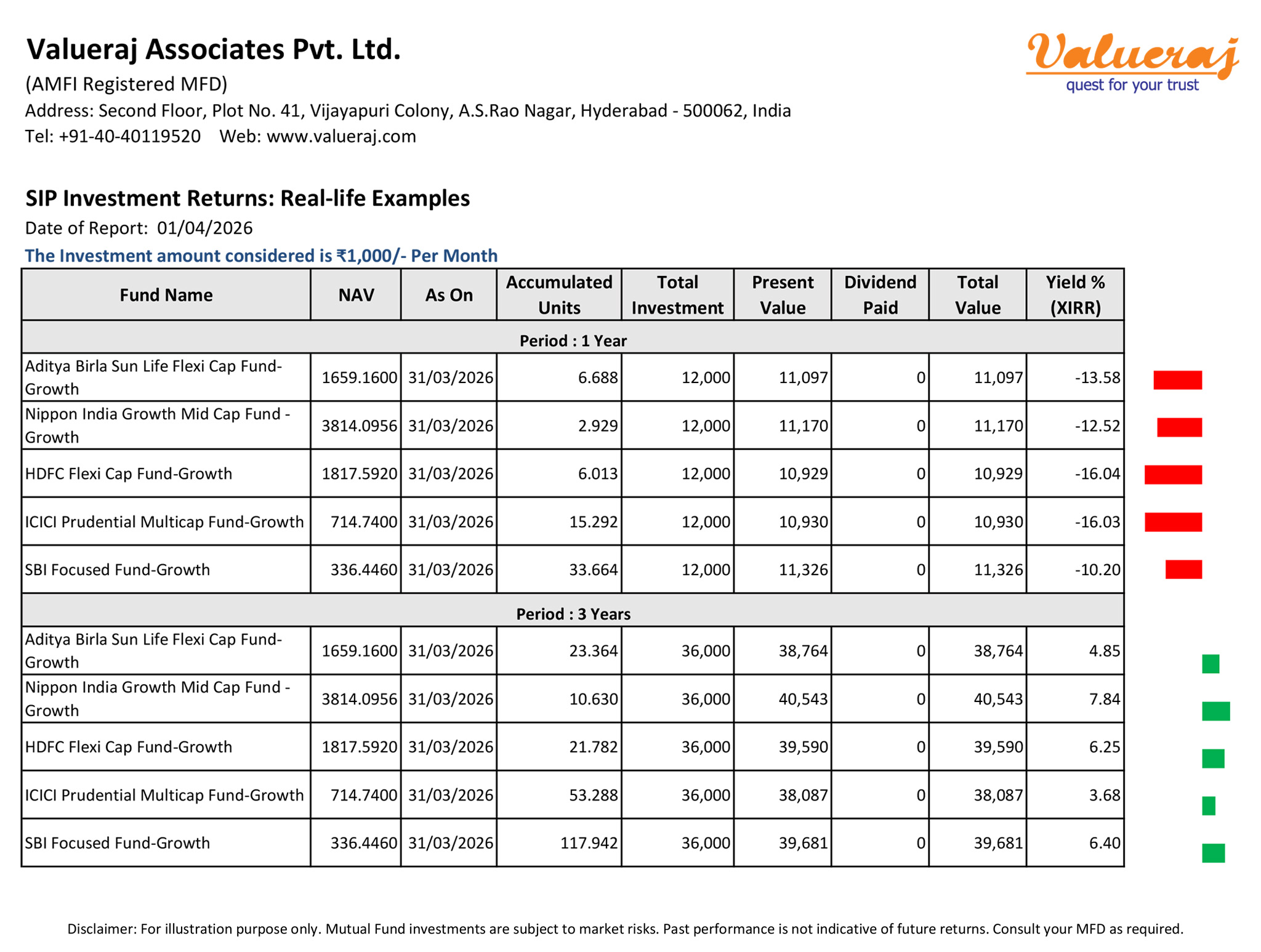

Investing fixed amount systematically at regular intervals is referred to as systematic investing. This mode of investing in equity mutual funds evens out the risk due to market volatility and facilitates discipline in investing regardless of ups and downs in the stock market. This enables higher returns by averaging out cost of investment in the long-term.

Find below the real-life returns of SIP investments in various equity mutual funds for different tenures.

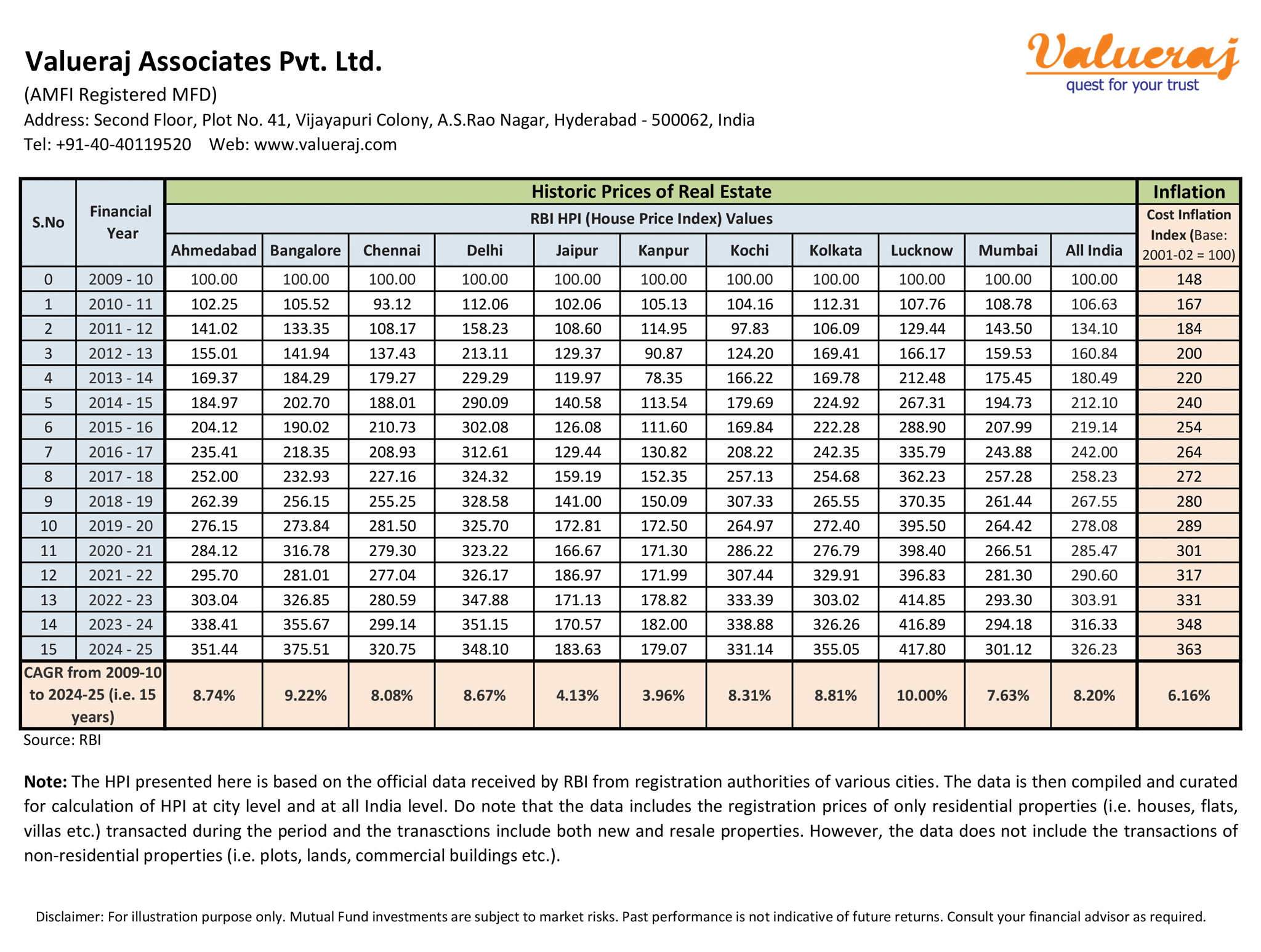

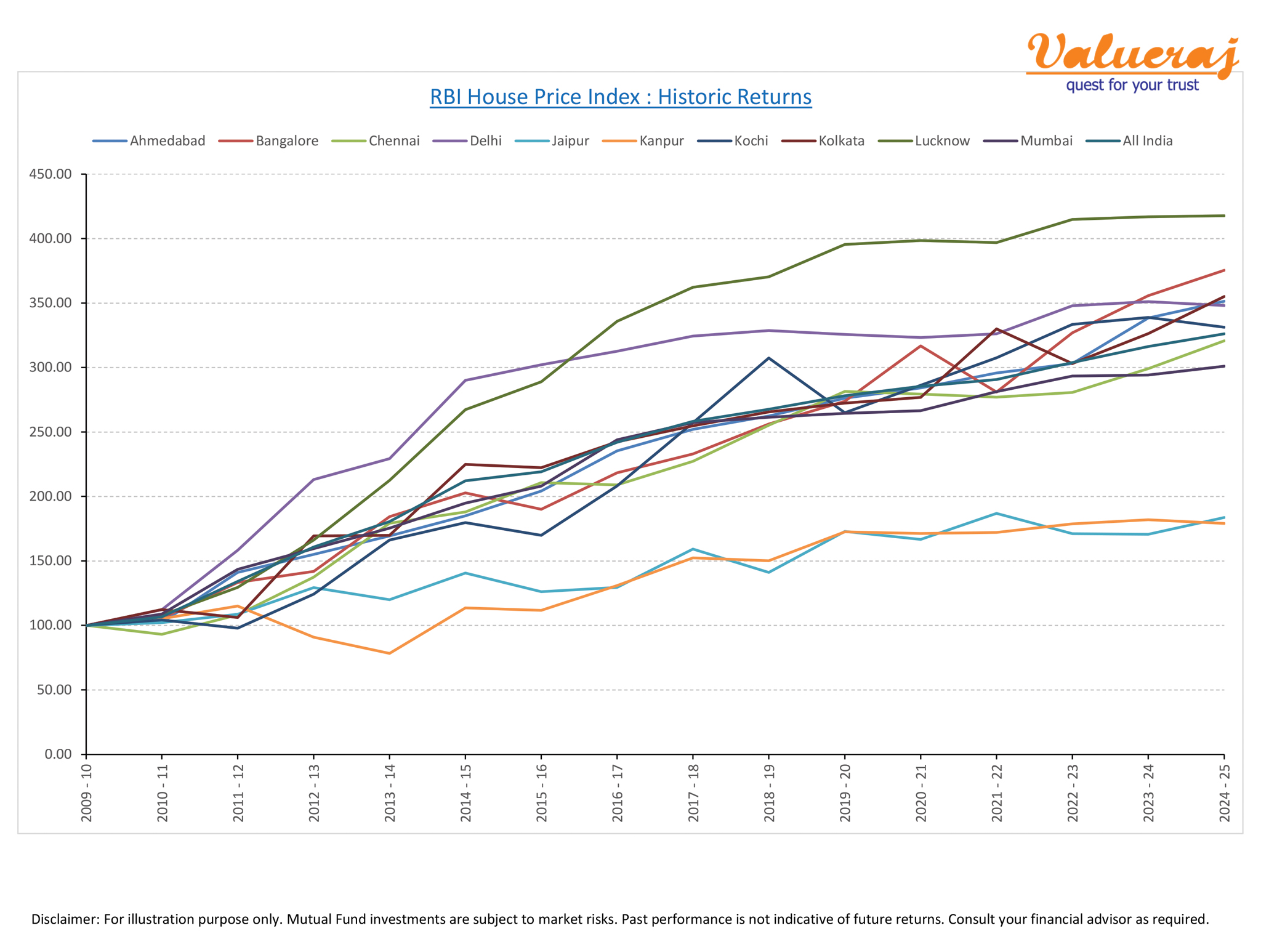

As like there are stock market indices such as Sensex/Nifty, there is House Price Index (HPI) for residential real estate market in India. This index is computed and published by RBI on quarterly basis. The historic data of this index indicates how the prices of residential properties have grown in recent years.

Find below the returns on real estate investments based on HPI for various cities across India.

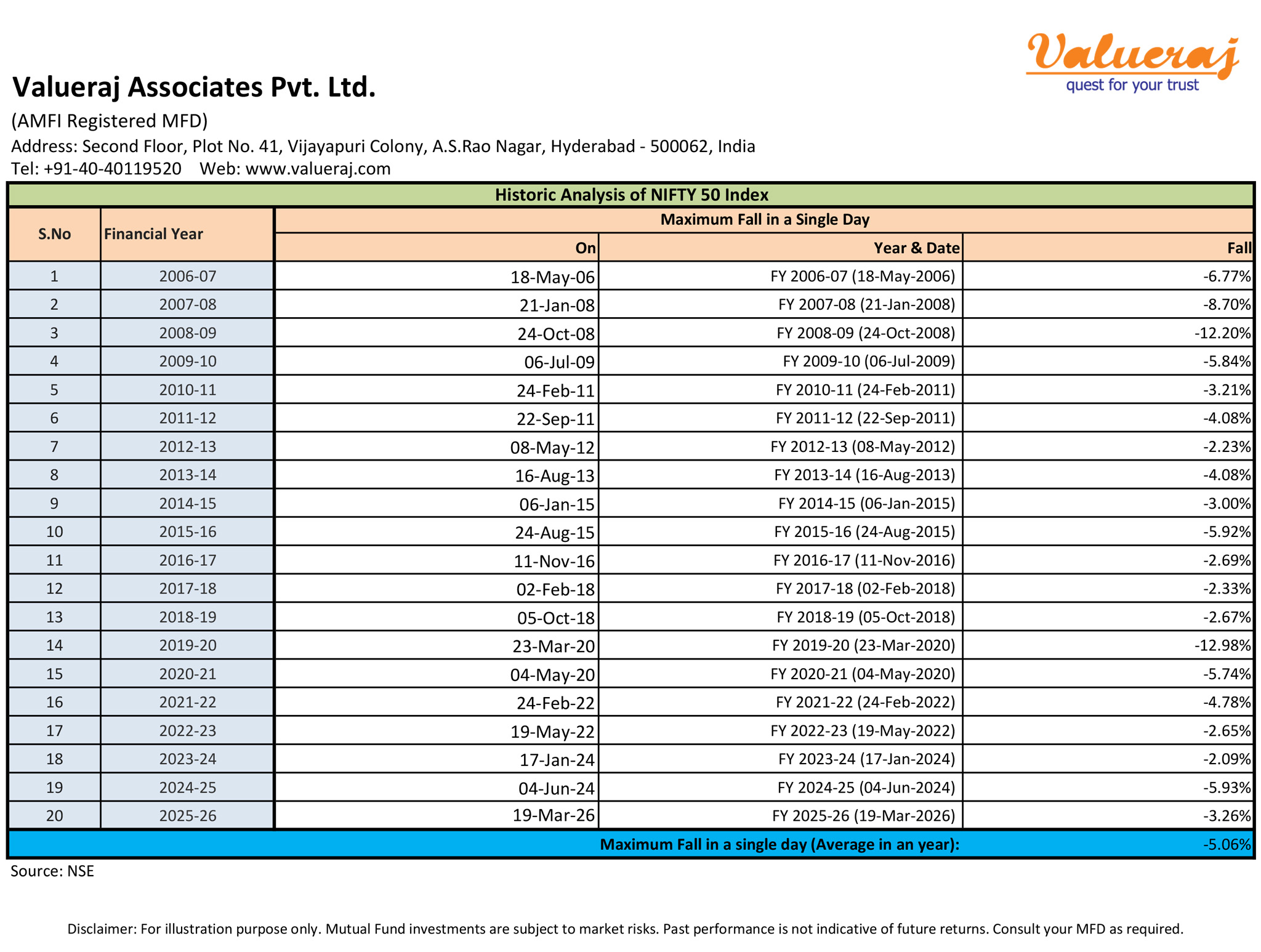

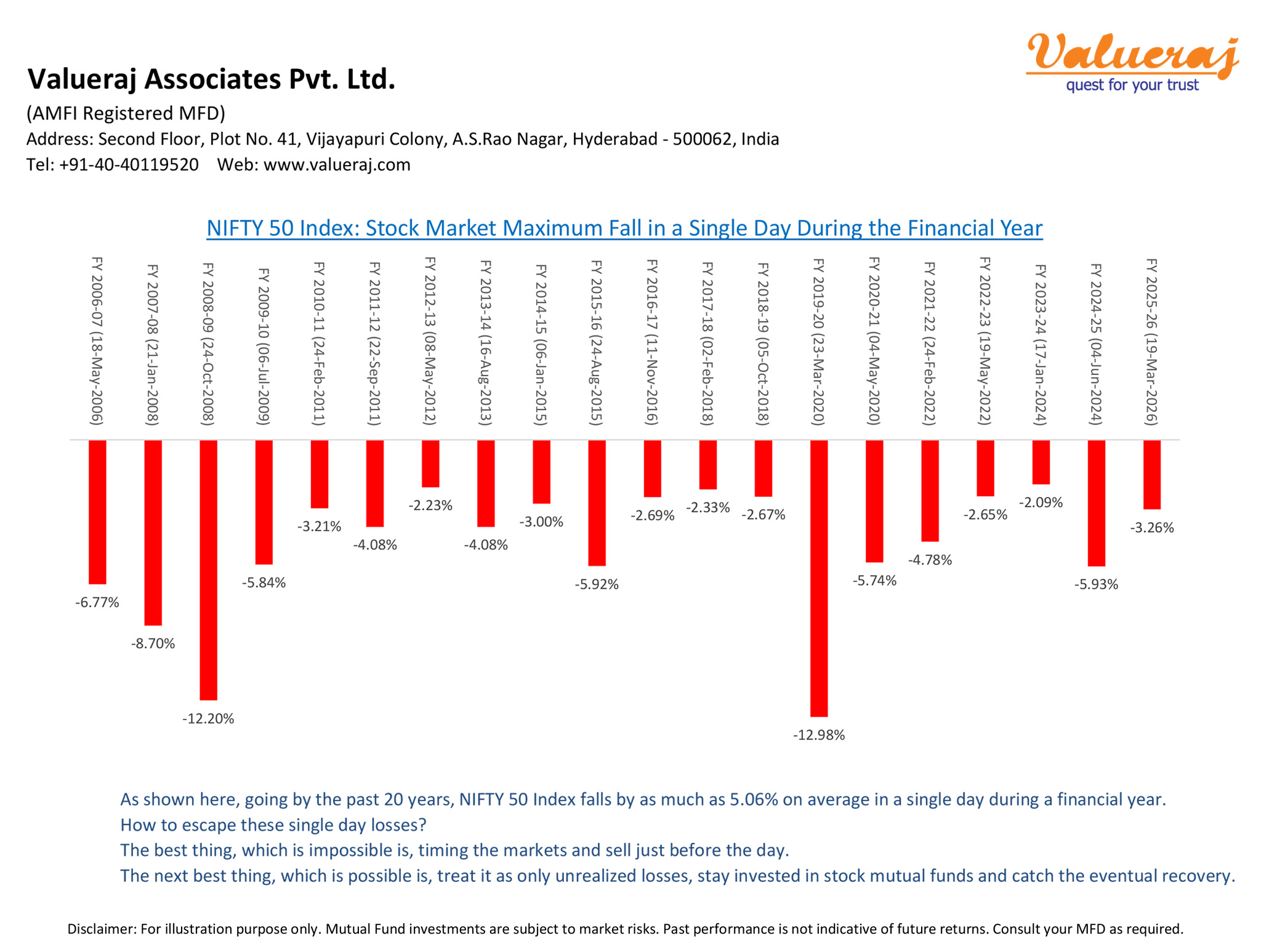

Stock markets may react violently to certain news/events. There can be sudden steep falls in a single day. However, you need not panic at such times as these could be momentary. Instead, stick to your investment plan, as the markets may recover eventually.

Find below the sudden single day falls of Nifty50 index in each financial year in the past 20 years.

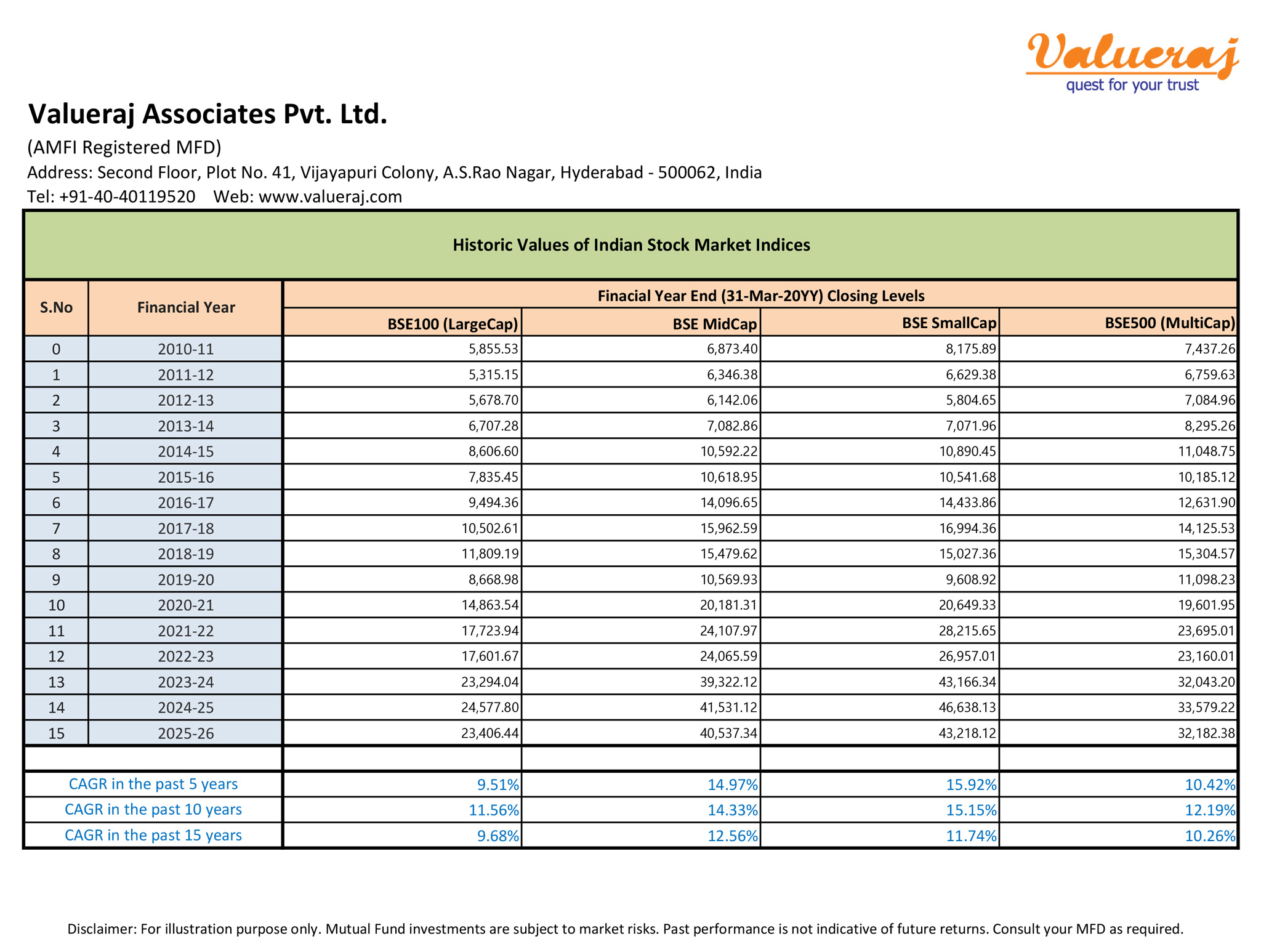

It is a common misconception that smallcap funds and midcap funds outperform largecap funds. However, there is no such outperformance on consistent basis across various tenures. Therefore, you better diversify your investments in stock funds representing all market caps.

Find below the historic returns of various market caps in India over last 15 years.

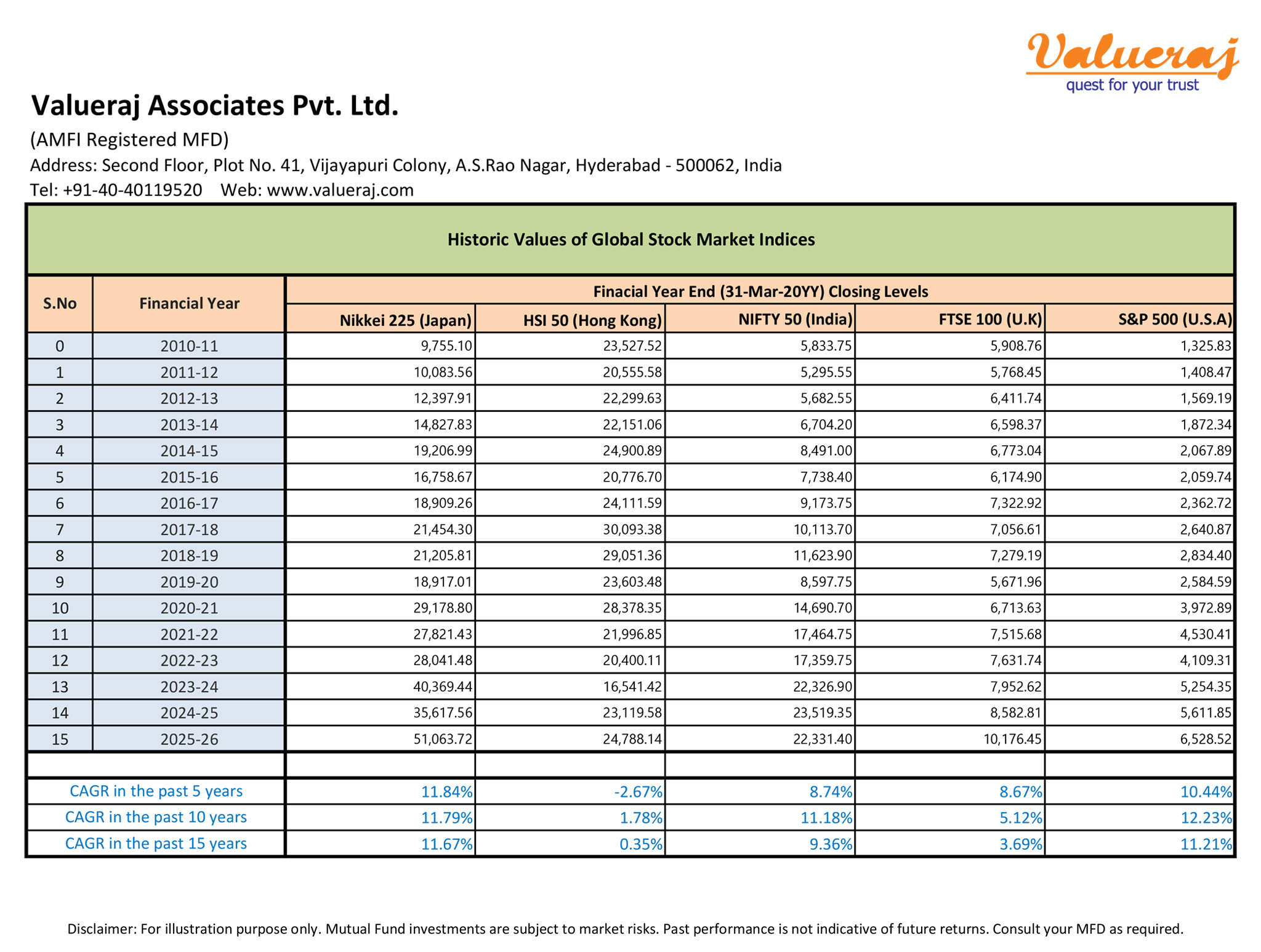

Global investing would no doubt gives you the opportunity to invest into other stock markets. However, this comes with risks related to regulatory changes, currency fluctuation and political instability in the respective countries. Moreover, there are instances of certain markets giving very low returns for prolonged periods of time.

Find below the performance analysis of four major global indices against Nifty50 over past 15 years.

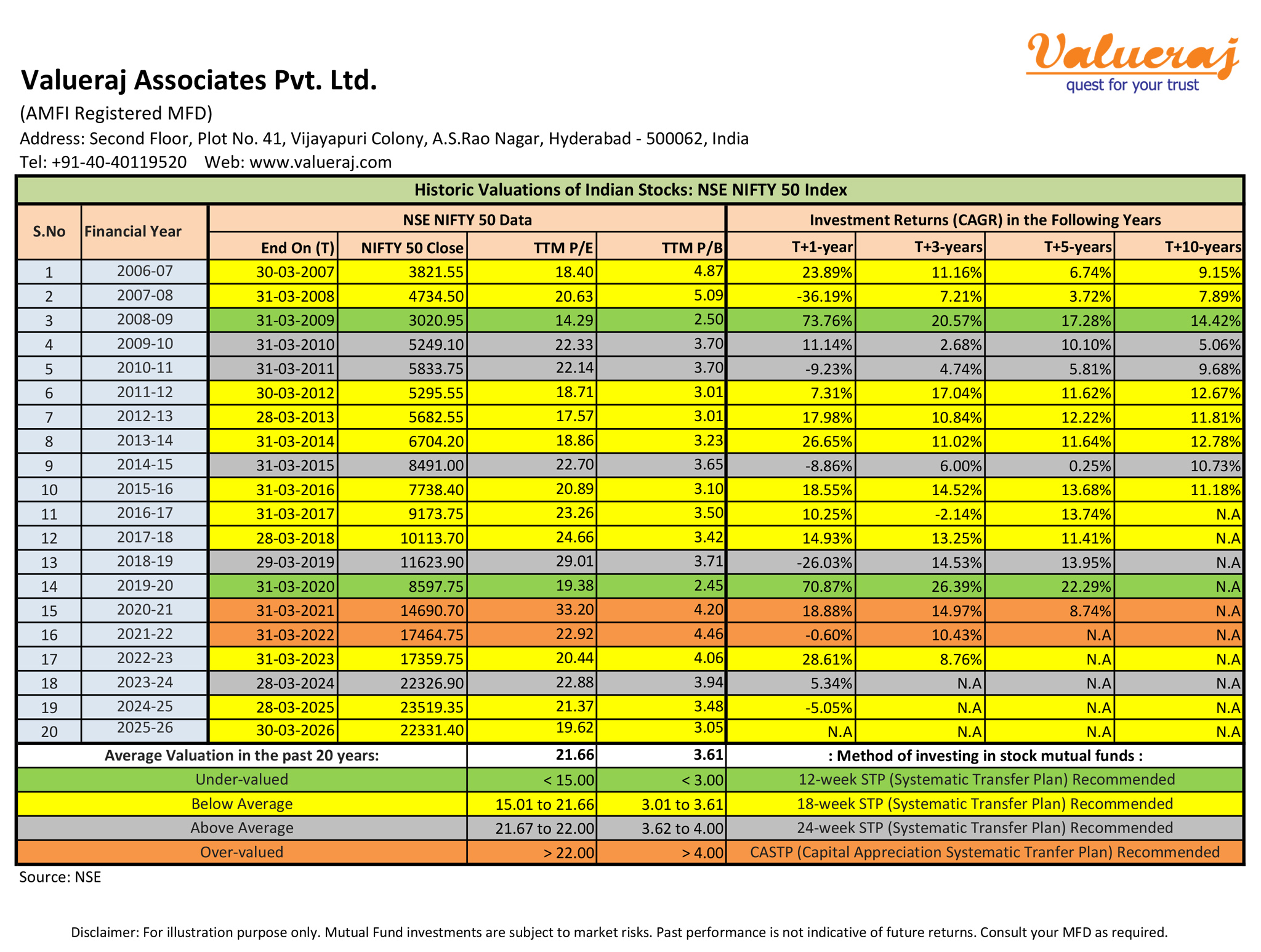

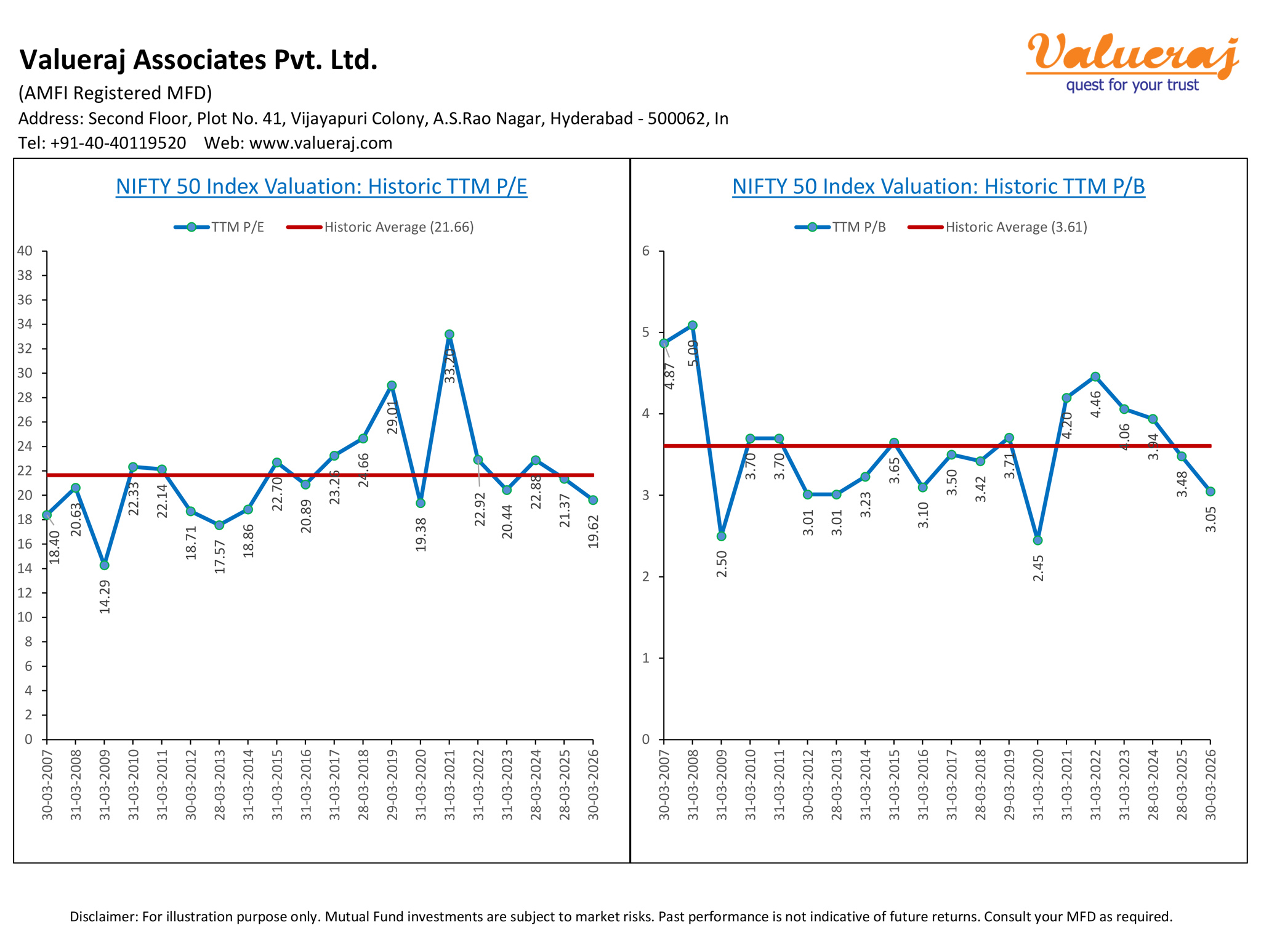

As a thumb rule, valuation of stock markets can be gauged using two fundamental ratios P/E (Price to Earnings) and P/B (Price to Book). Generally, stock markets are considered to be undervalued when Nifty50 index P/E is less than 15 or P/B is less than 3. Likewise, stock markets are considered to overvalued when Nifty50 index P/E is more than 22 or P/B is more than 4.

Find below our analysis on historic P/E and P/B values of Nifty50 index over past 20 years.

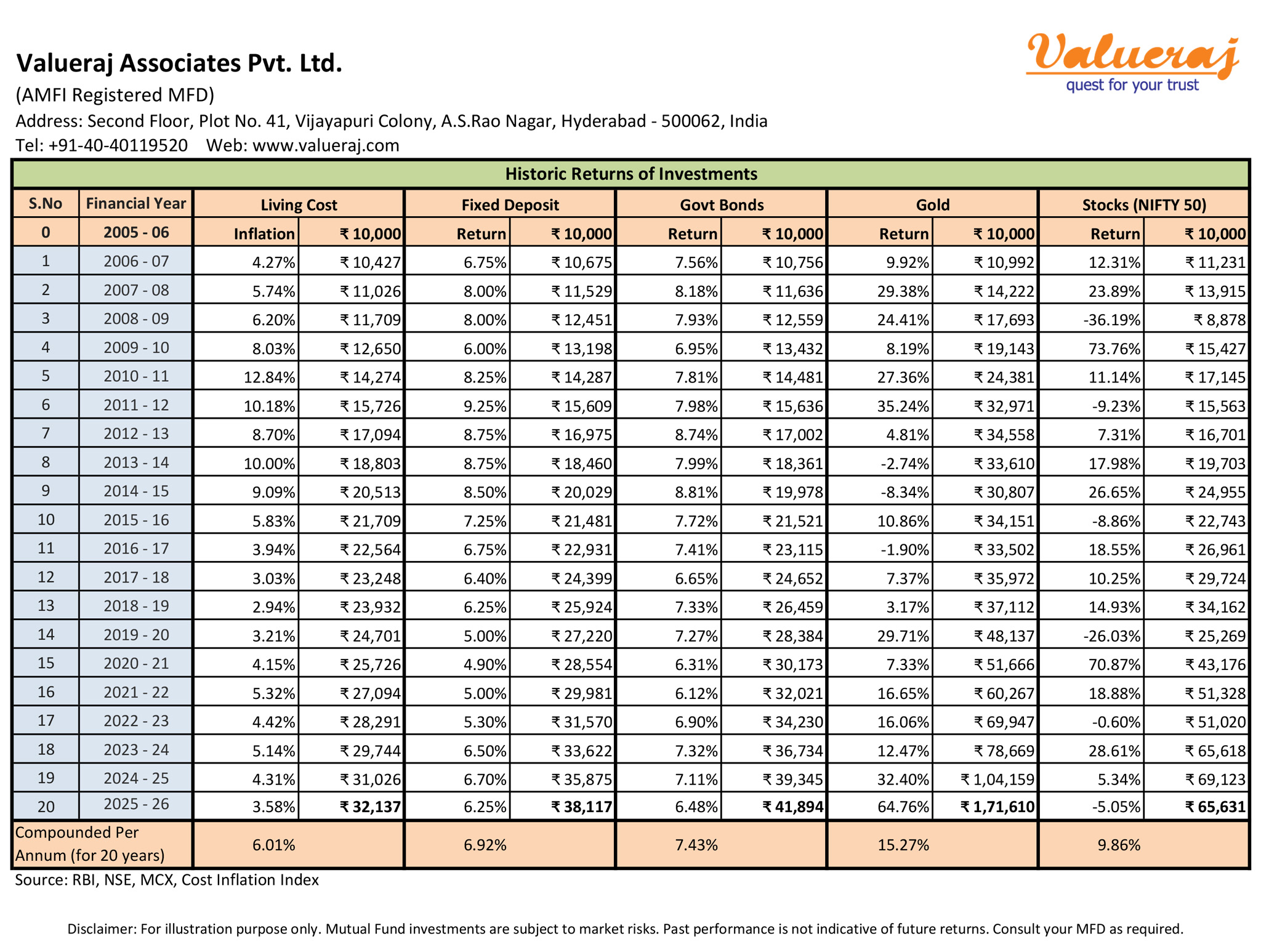

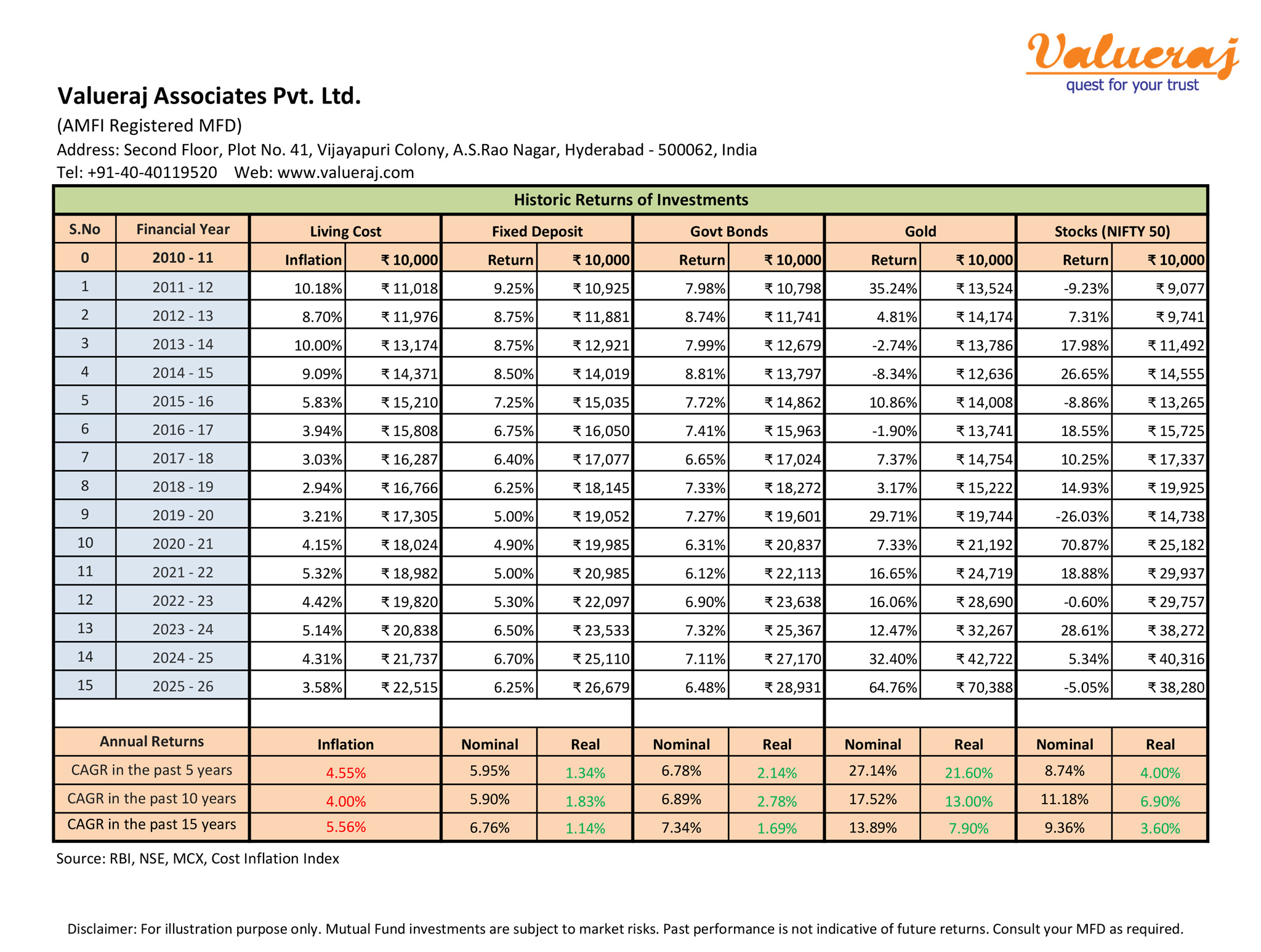

In investing, lower the risk lower the return and higher the risk higher the return. Investments in Stocks and Gold come with higher risk as compared to FDs and Bonds. To commensurate with this risk, Stocks and Gold give higher returns as compared to FDs and Bonds.

Find below our analysis on historic returns of various asset classes in India over last 20 years.

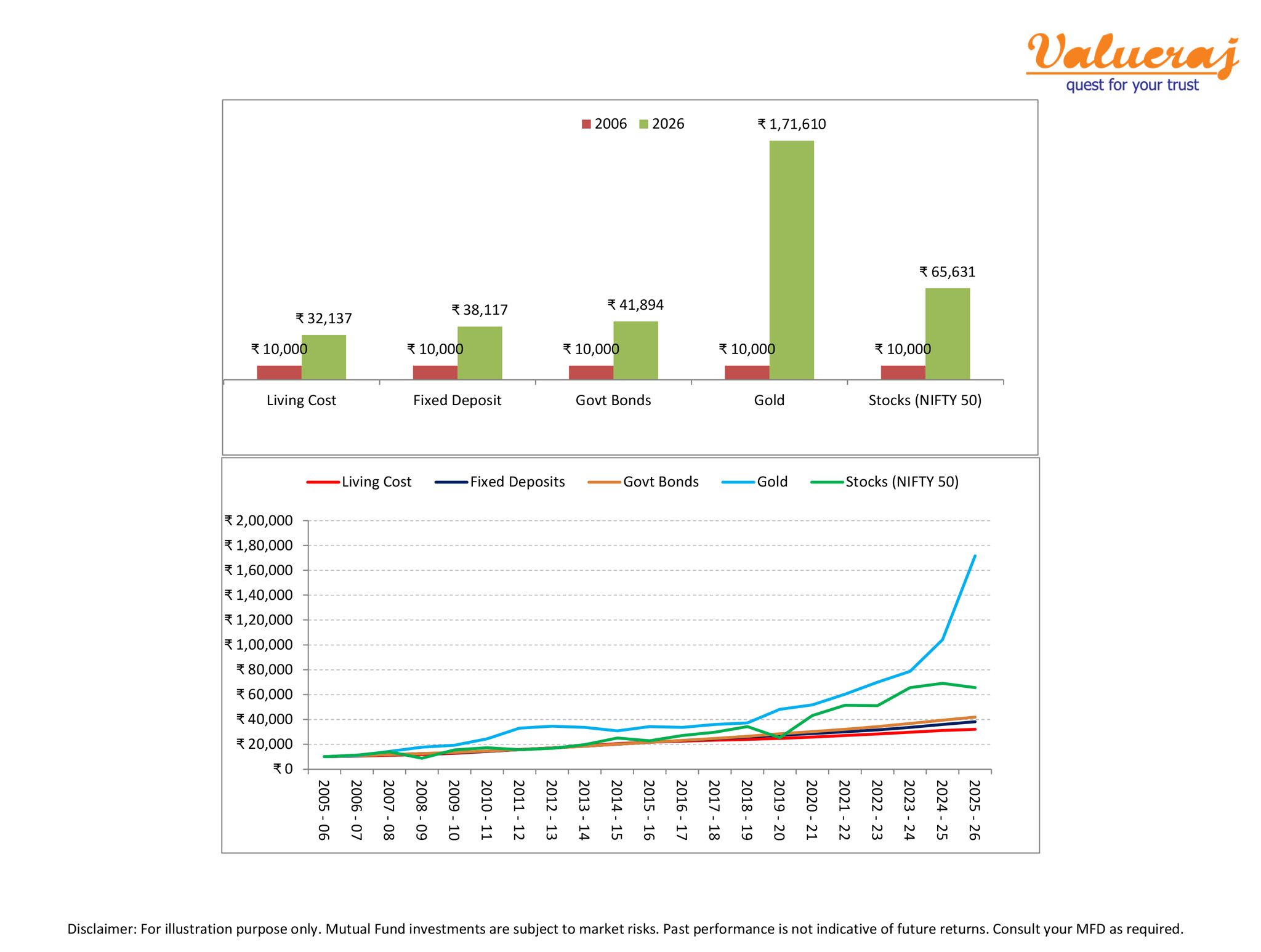

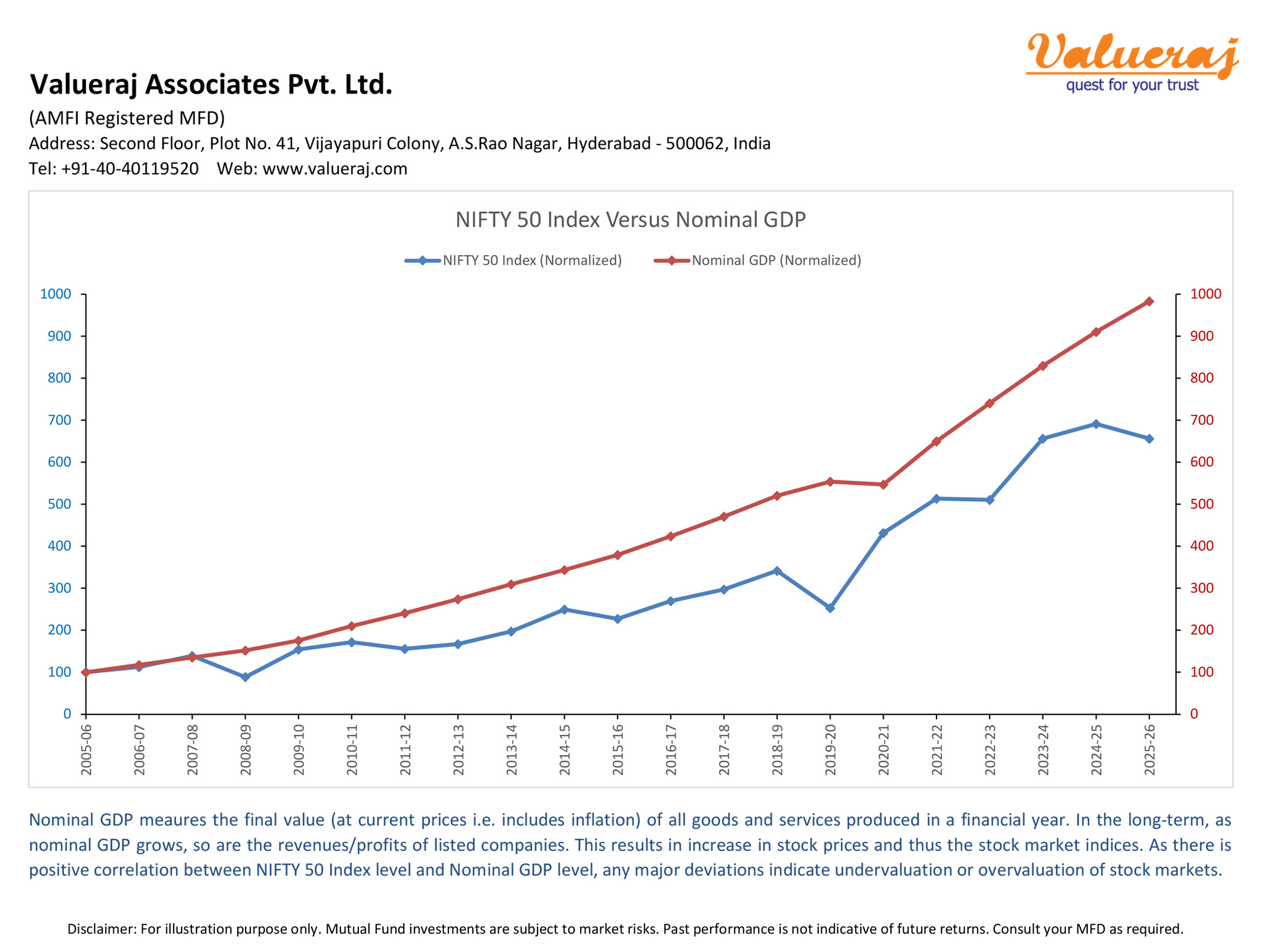

India is one of the fastest growing economies in the world and its nominal GDP (Gross Domestic Product) is expected to reach $5 trillion in the next few years. As the nominal GDP grows, the revenues/profits of listed companies also grow. This results in increase in stock prices and thus the stock market indices.

Find below our analysis on historic growth of India’s nominal GDP and historic returns of Nifty50 index in the past 20 years.

The return you get on any investment is called Nominal Return. After adjusting for Inflation in this Nominal Return, you get Real Return. Actually, it is the Real Return that generates true additional wealth for you.

As you know, Stocks and Gold give higher nominal returns as compared to FDs and Bonds. Likewise, after adjusting for inflation, Stocks and Gold give higher real returns as compared to FDs and Bonds.

Find below our analysis on historic real returns of various asset classes in India over last 15 years.

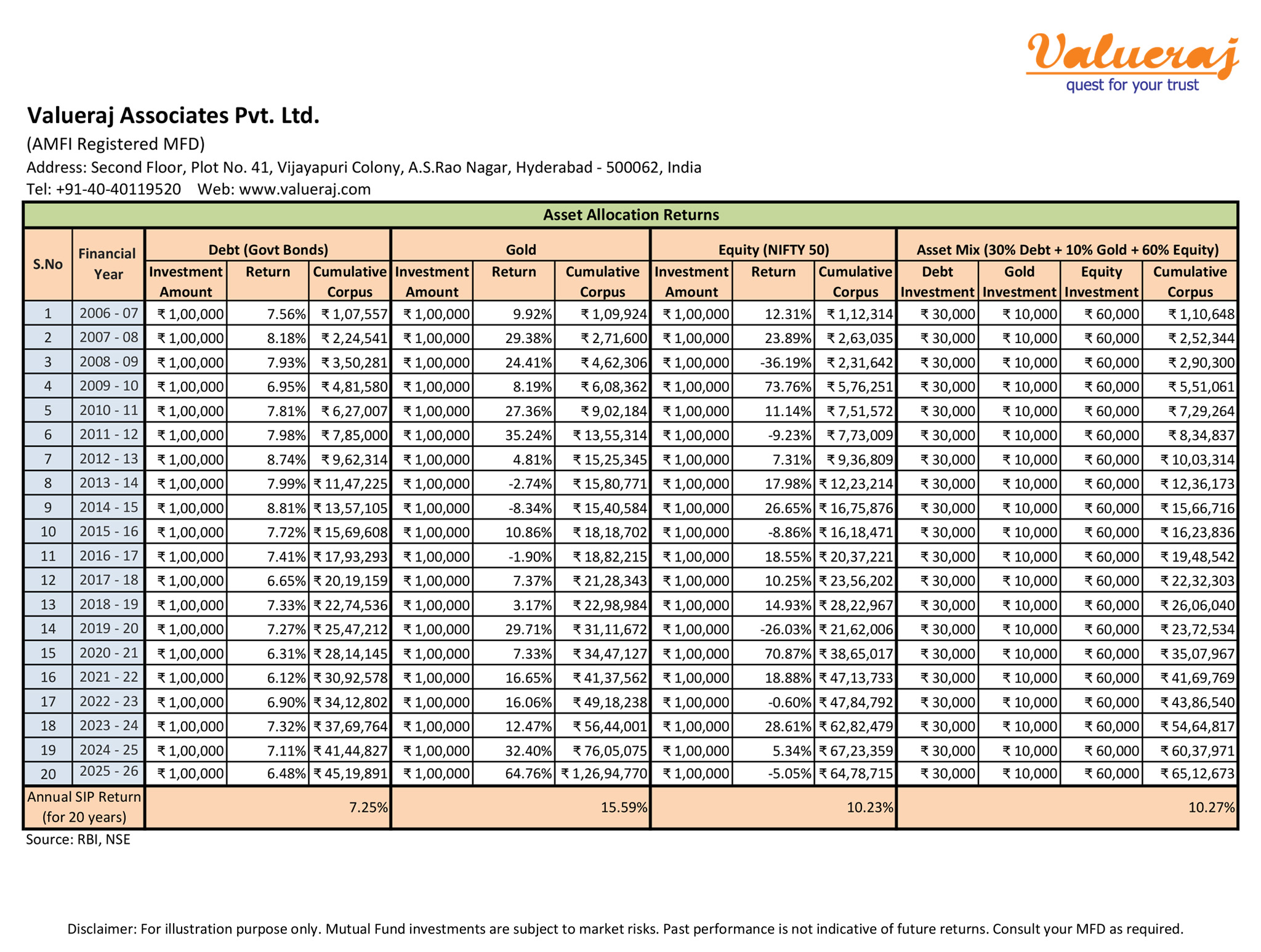

Asset Allocation means investing in various asset classes in right proportions to get optimal risk adjusted returns in your portfolio.

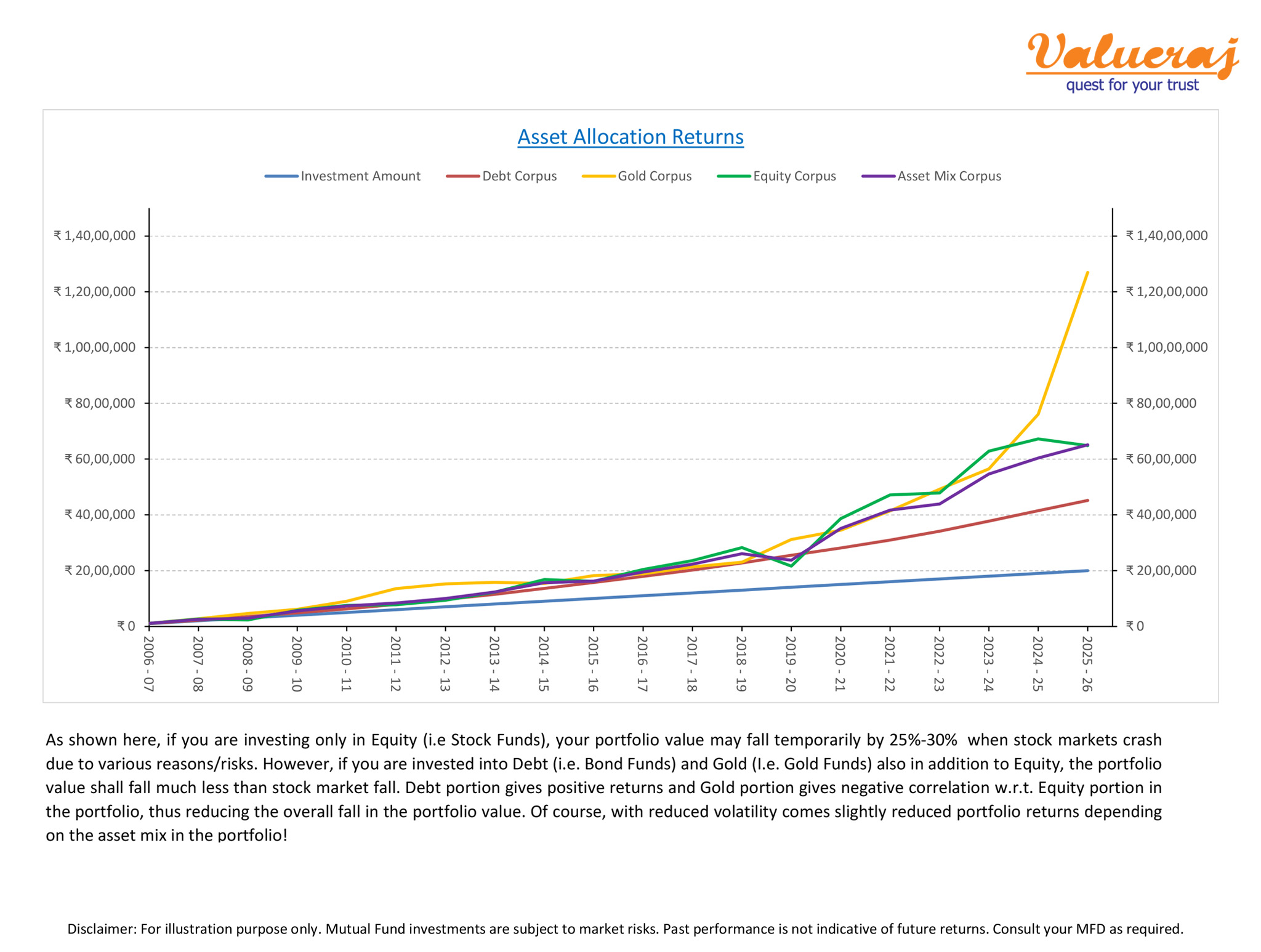

In essence, if you are investing only in Equity, your portfolio value may fall temporarily by 25%-30% when stock markets crash due to various reasons/risks. However, if you are invested into Debt and Gold also in addition to Equity, the portfolio value shall fall much less than stock market fall. Debt portion gives positive returns and Gold portion gives negative correlation w.r.t. Equity portion in the portfolio, thus reducing the overall fall in the portfolio value.

For example, find below our analysis on historic retuns of SIP investments in individual asset classes vis-à-vis a portfolio with asset allocation of Debt:Gold:Equity in 30:10:60 mix.

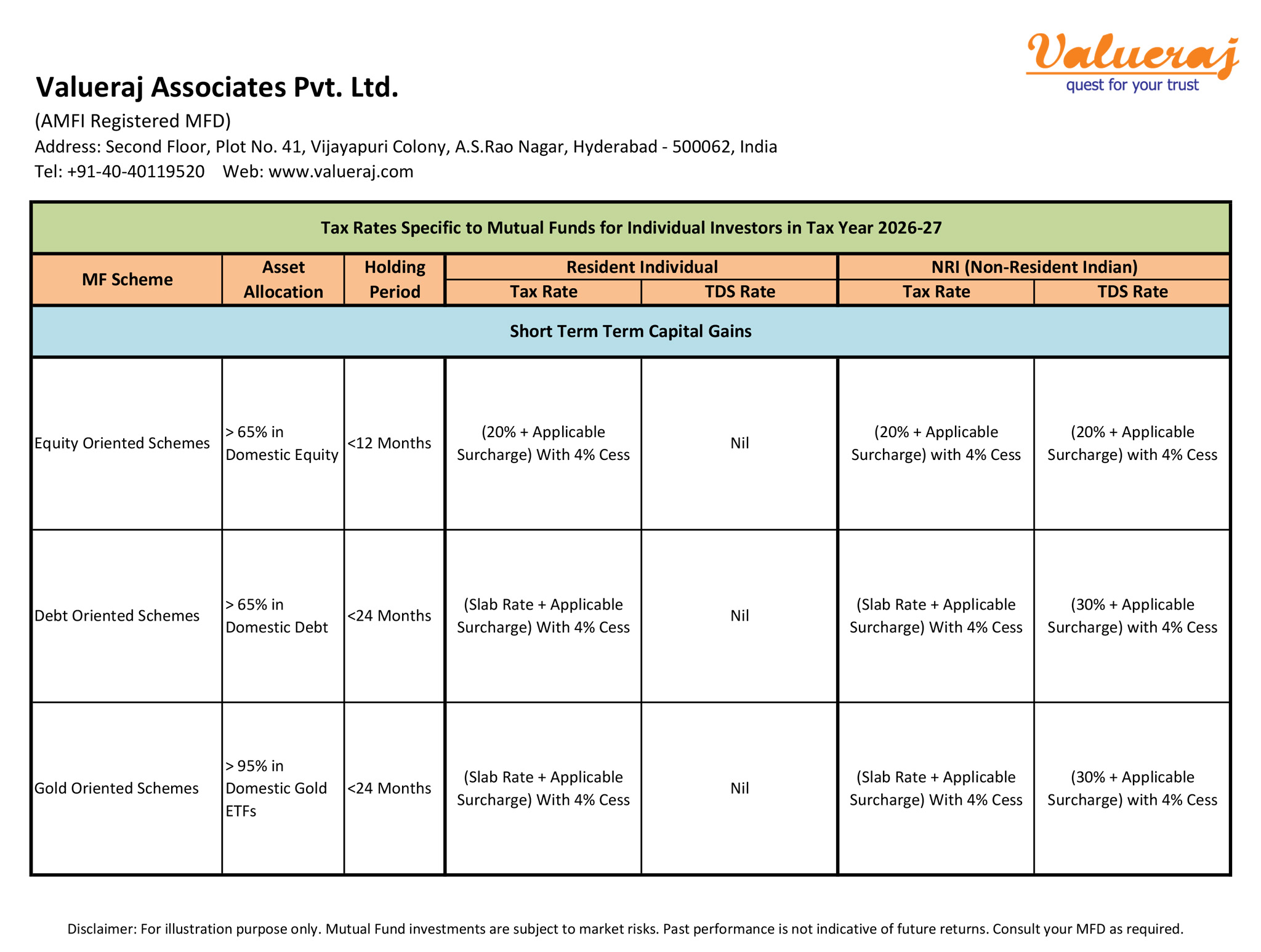

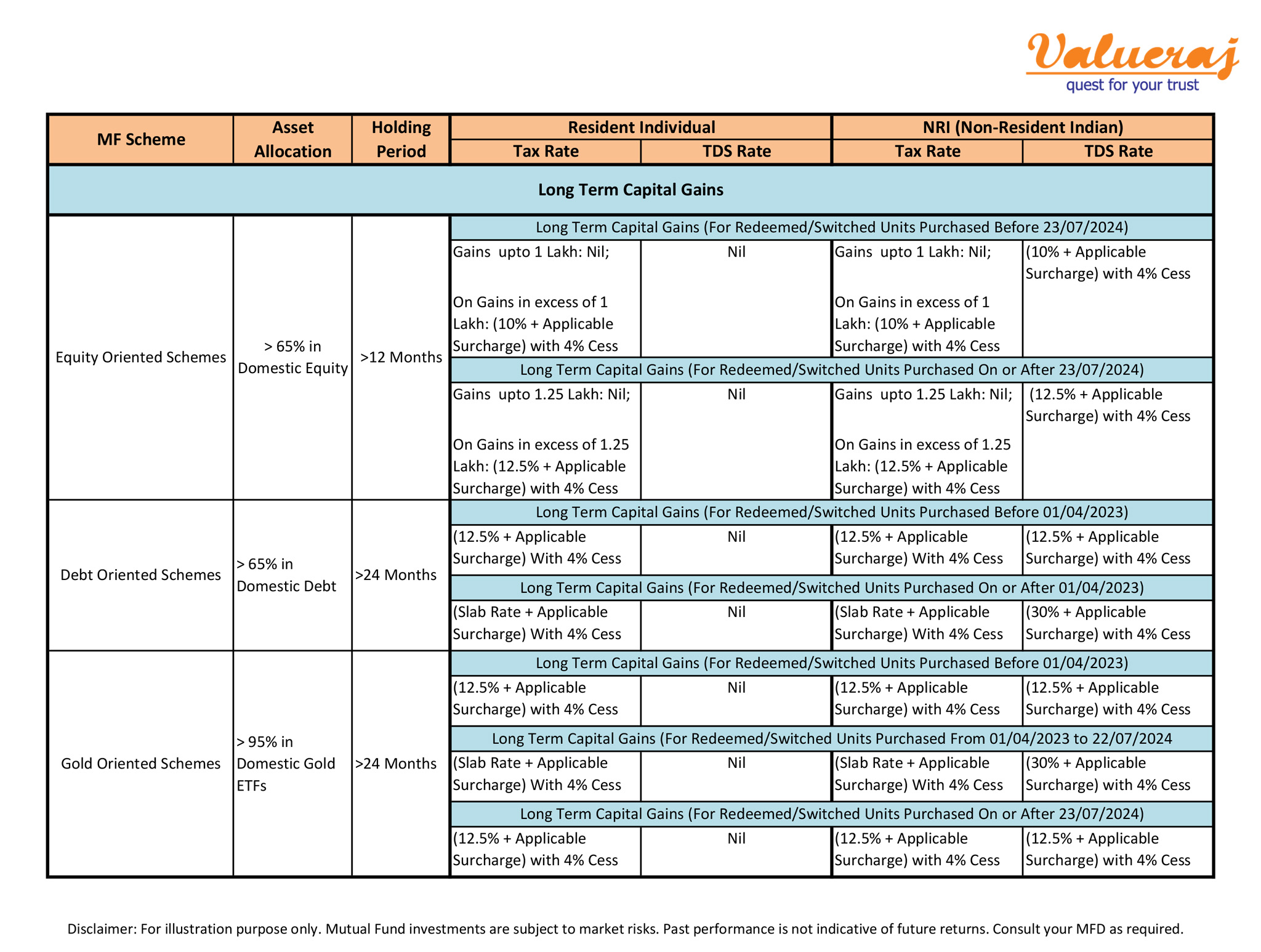

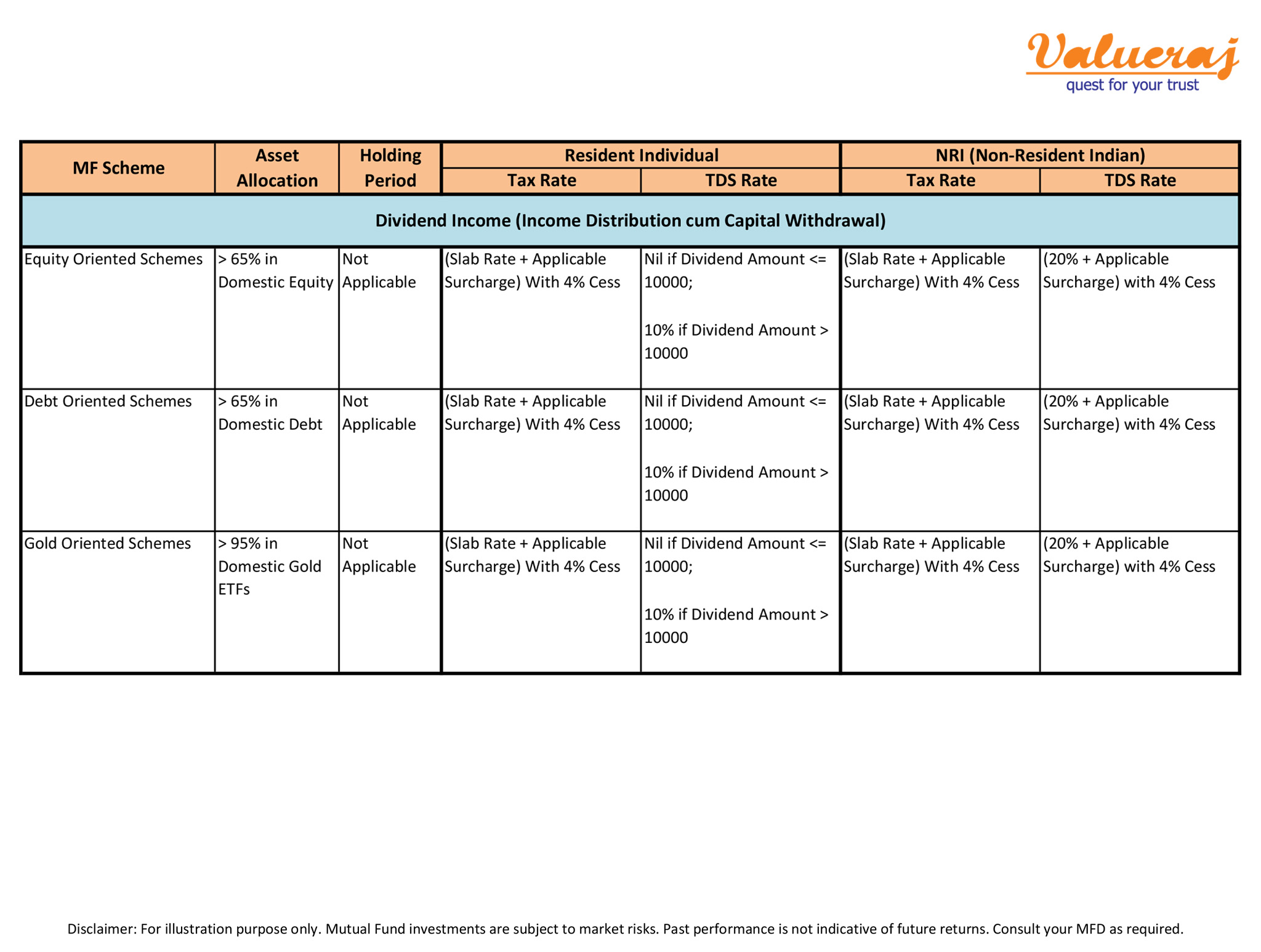

When you invest in Mutual Funds, you realize Capital Gains at the time of sale. Also, if you opt for dividend option at the time of investment, you receive dividend income at regular intervals. Both Capital Gains and Dividend Income are liable for taxes.

For your reference, find below the Tax Rates and TDS Rates specific to mutual funds for individual investors.

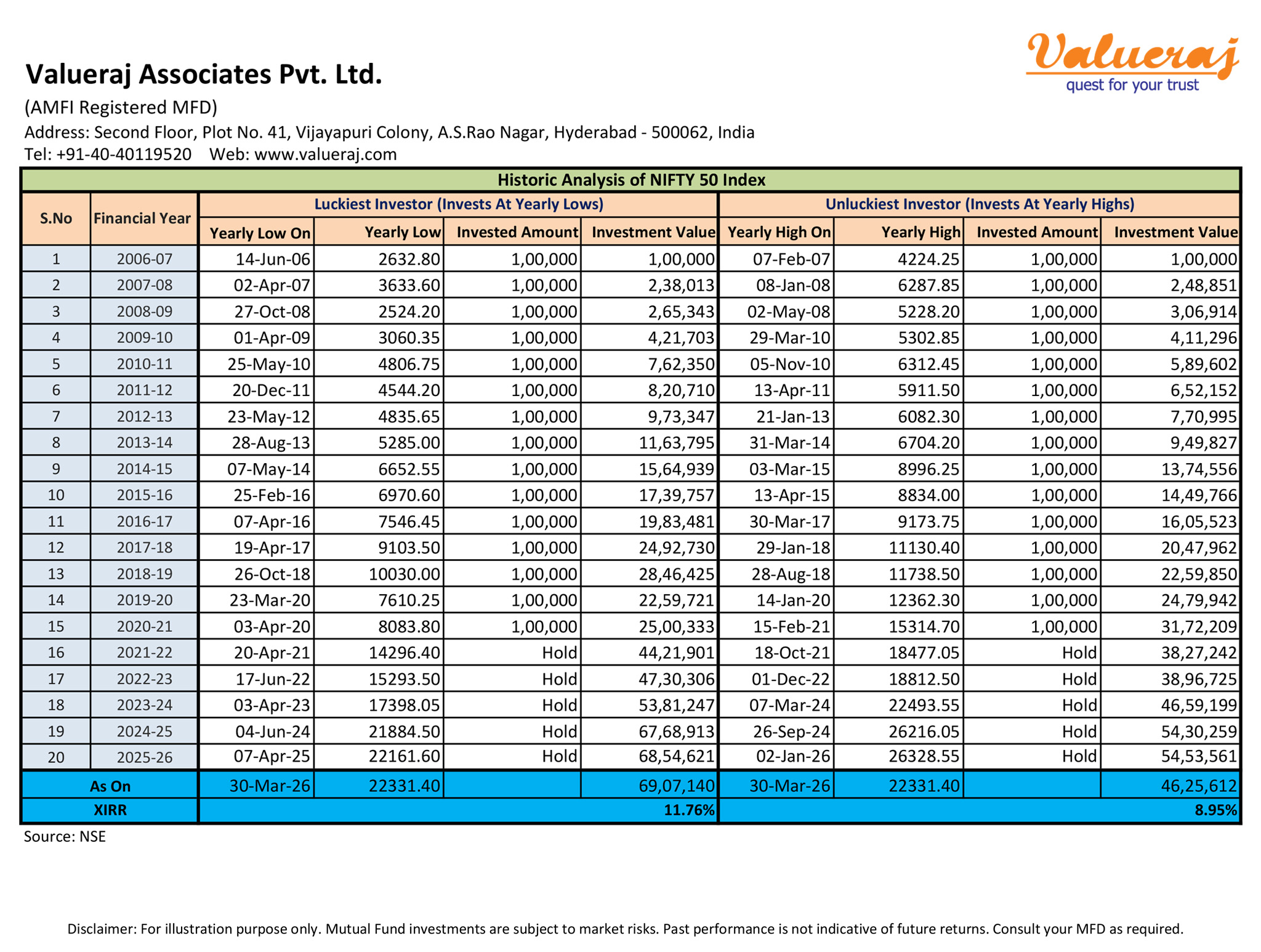

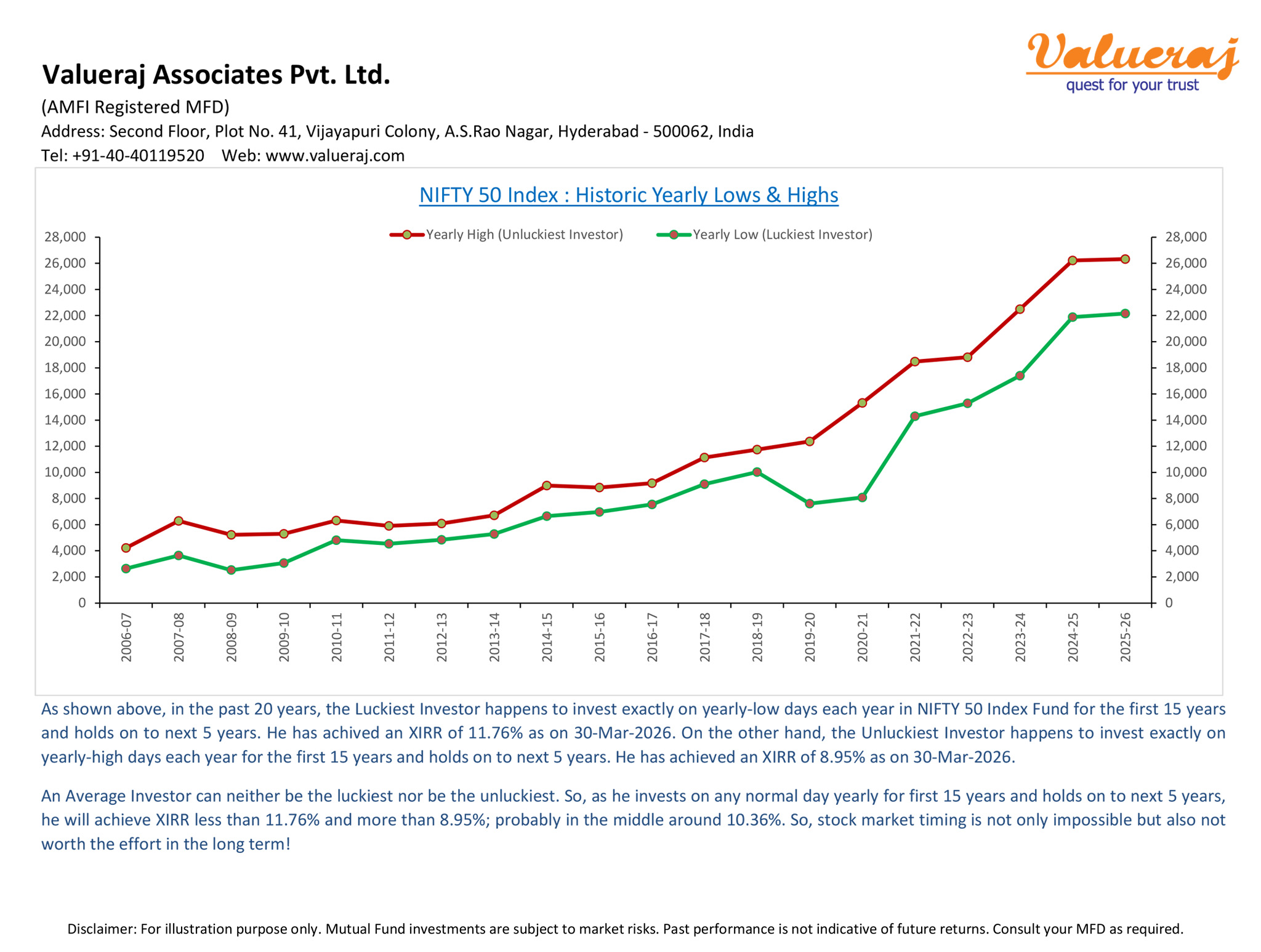

As stock markets are inherently volatile, there are yearly-low days and yearly-high days in every year. One has to be the luckiest investor to invest on yearly-low days every year. Similarly, one has to be the unluckiest investor to invest on yearly-high days every year. Even then, subject to investing for long-term, the extra return is not much for luckiest investor as compared to unluckiest investor. In fact, the unluckiness of the latter can be simpy countered by just holding for long-term. So, if you are investing for long-term, then market timing is just not worth trying.

Find below our analysis on historic returns of the luckiest investor and unluckiest investor in the past 20 years wherein they invested yearly for the first 15 years and then just held on for the next 5 years.

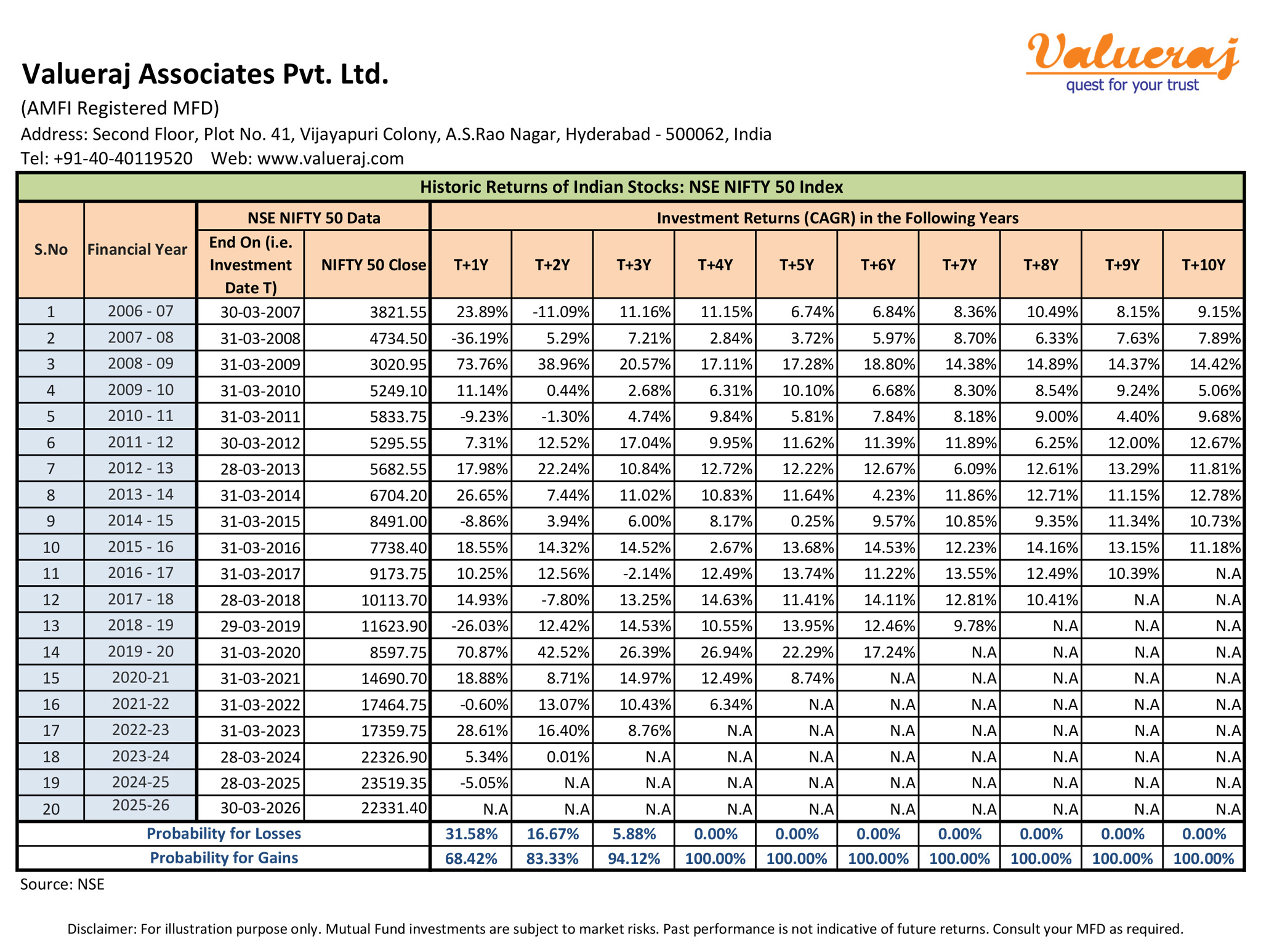

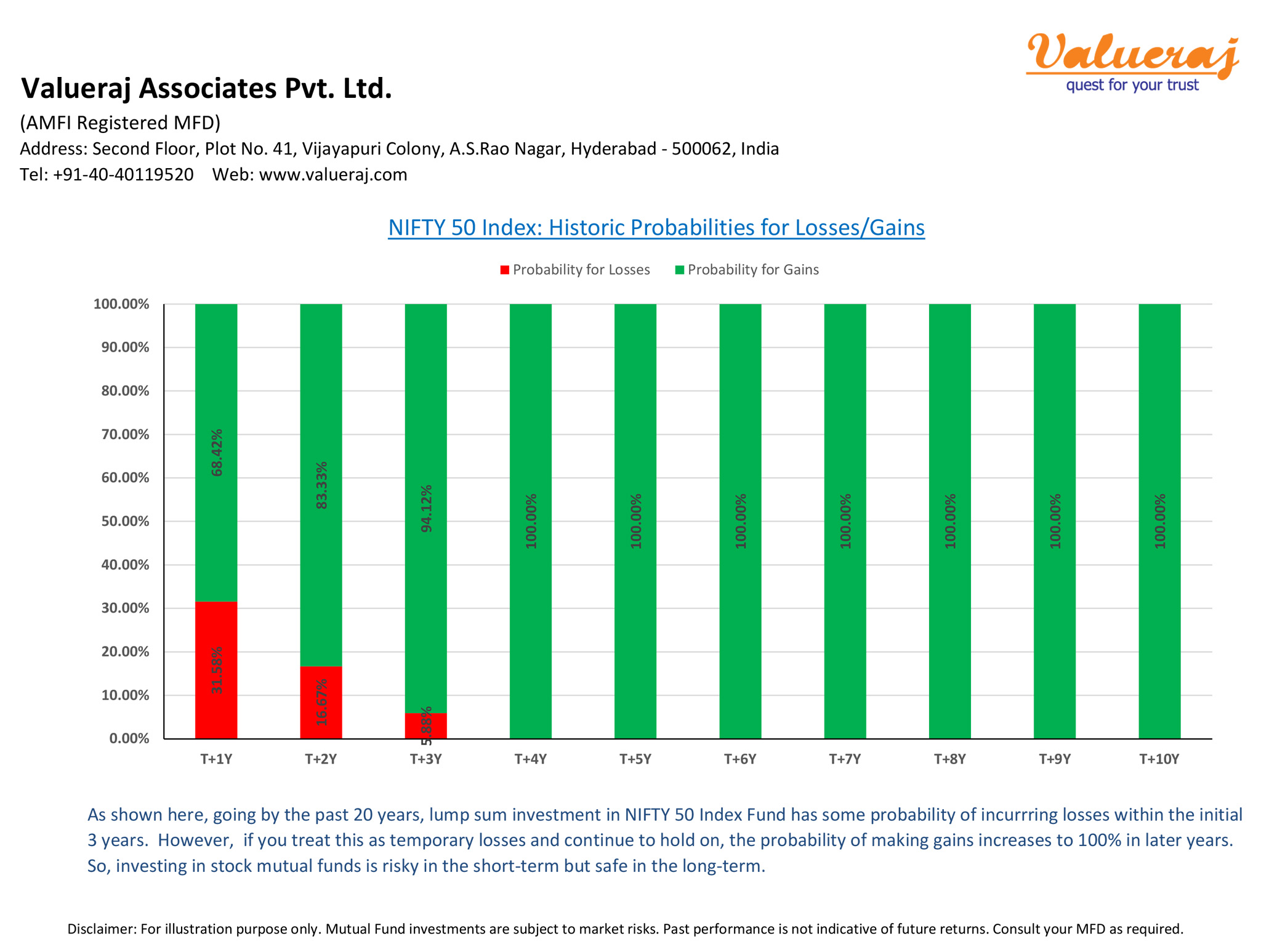

Investing in stock mutual funds is risky. But, the truth is, holding period is the antidote to that risk. Stock markets go through bullish phases and bearish phases. If invested during bullish phase, there is some probability of making losses in the short-term. However, if you ignore these temporary losses and continue to hold on, the probability of making gains becomes 100% in the long-term.

Find below our analysis on historic probabilities of NIFTY50 Index making losses/gains in subsequent years in the past 20 years.

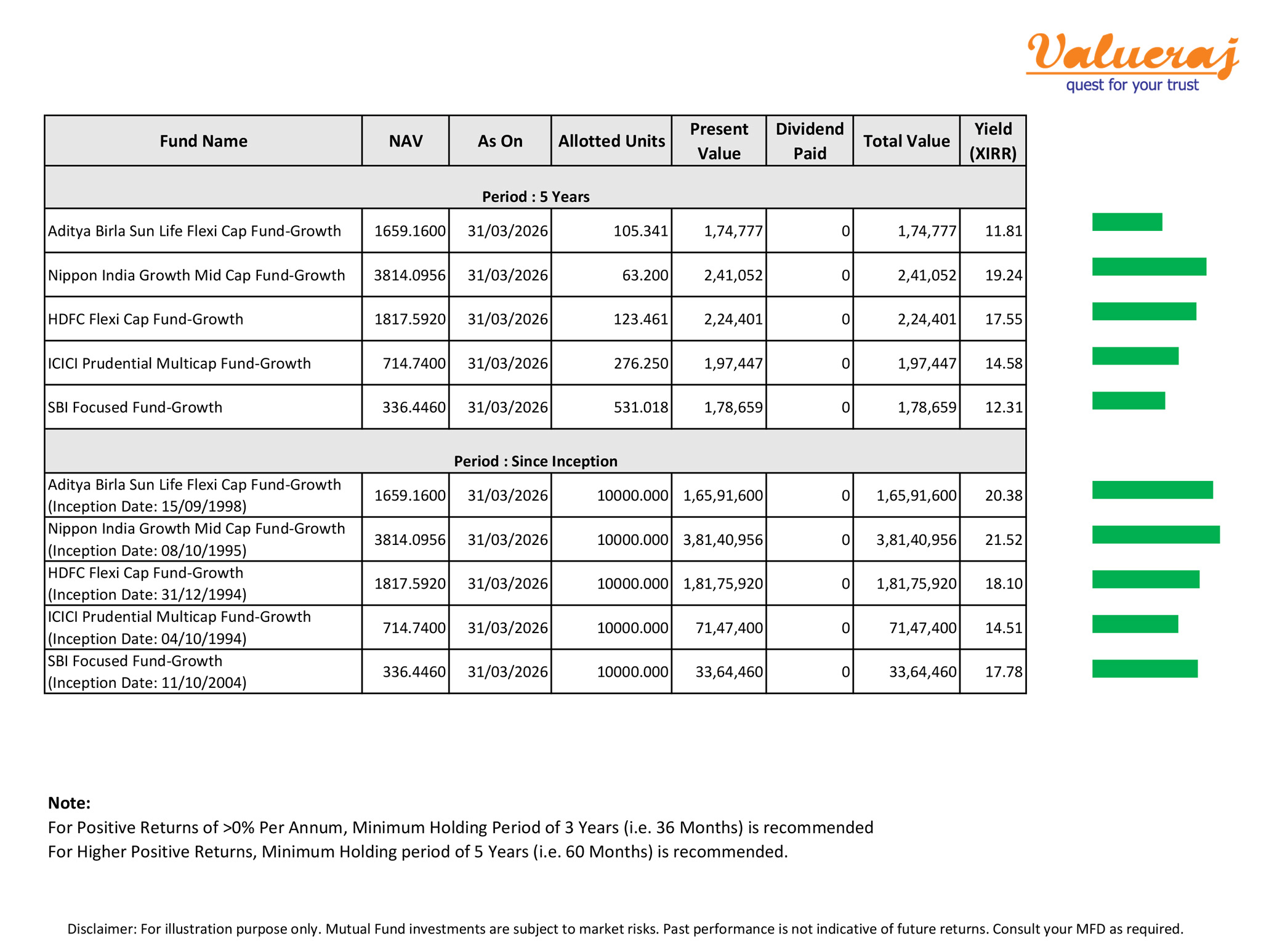

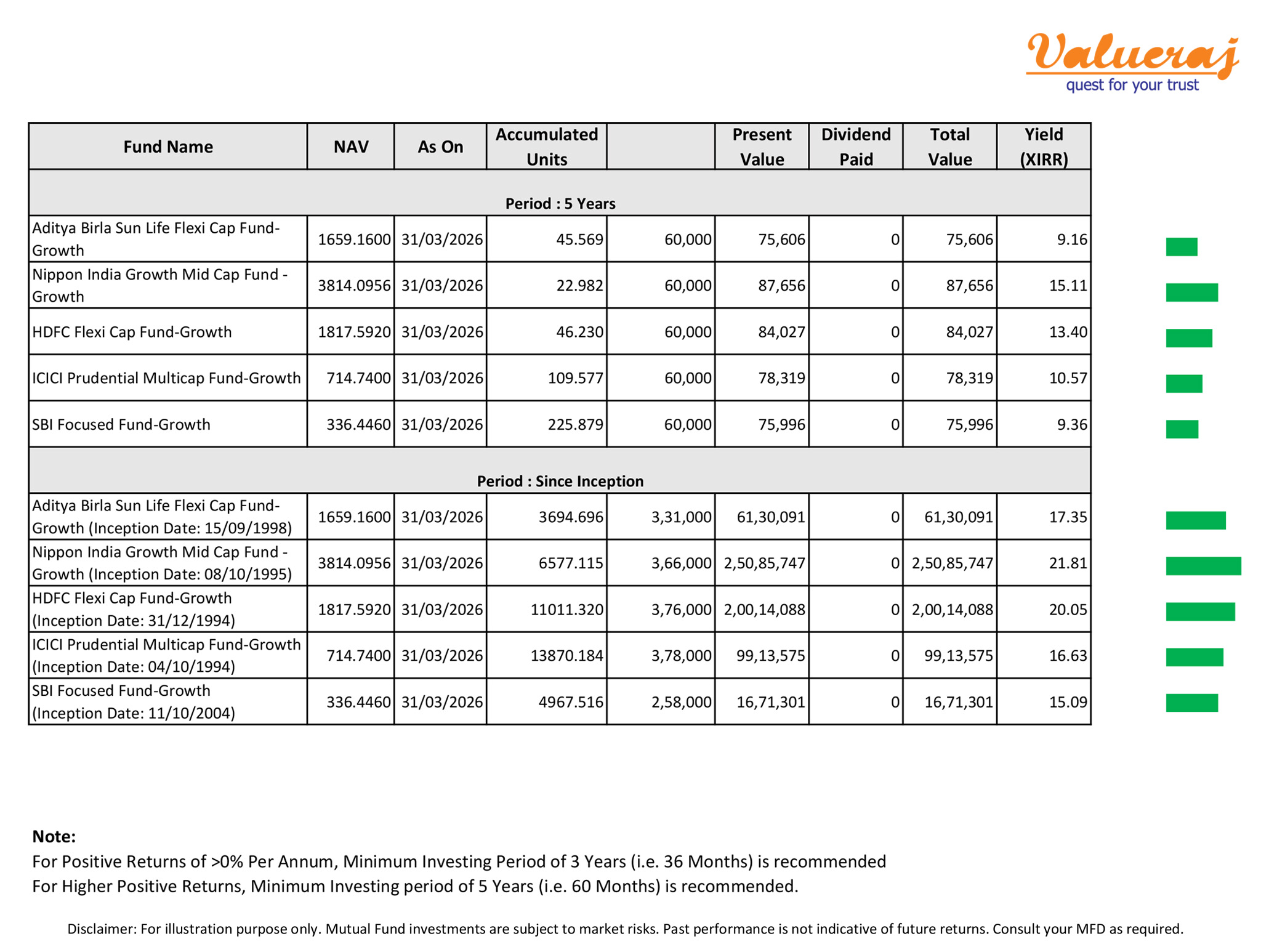

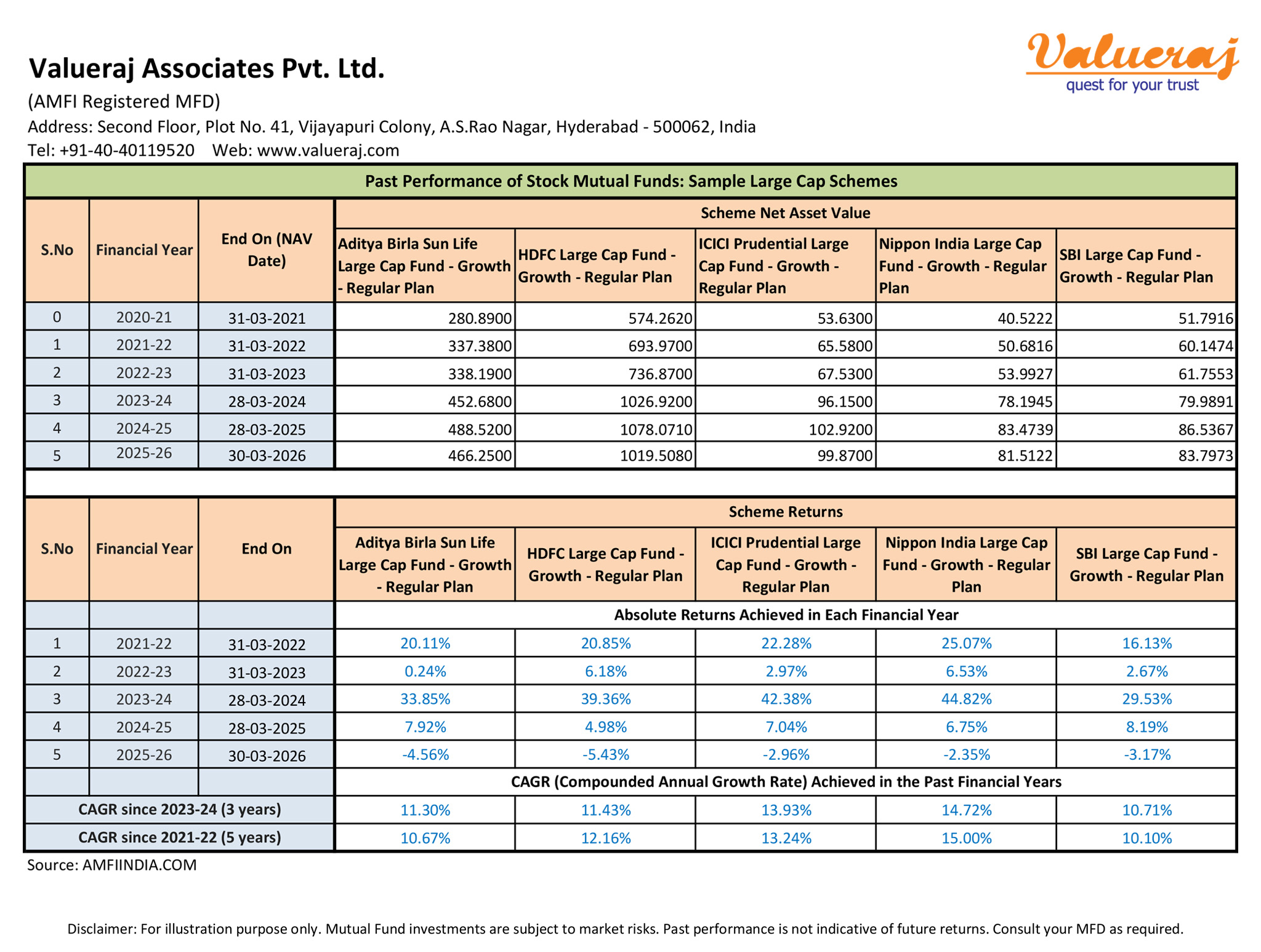

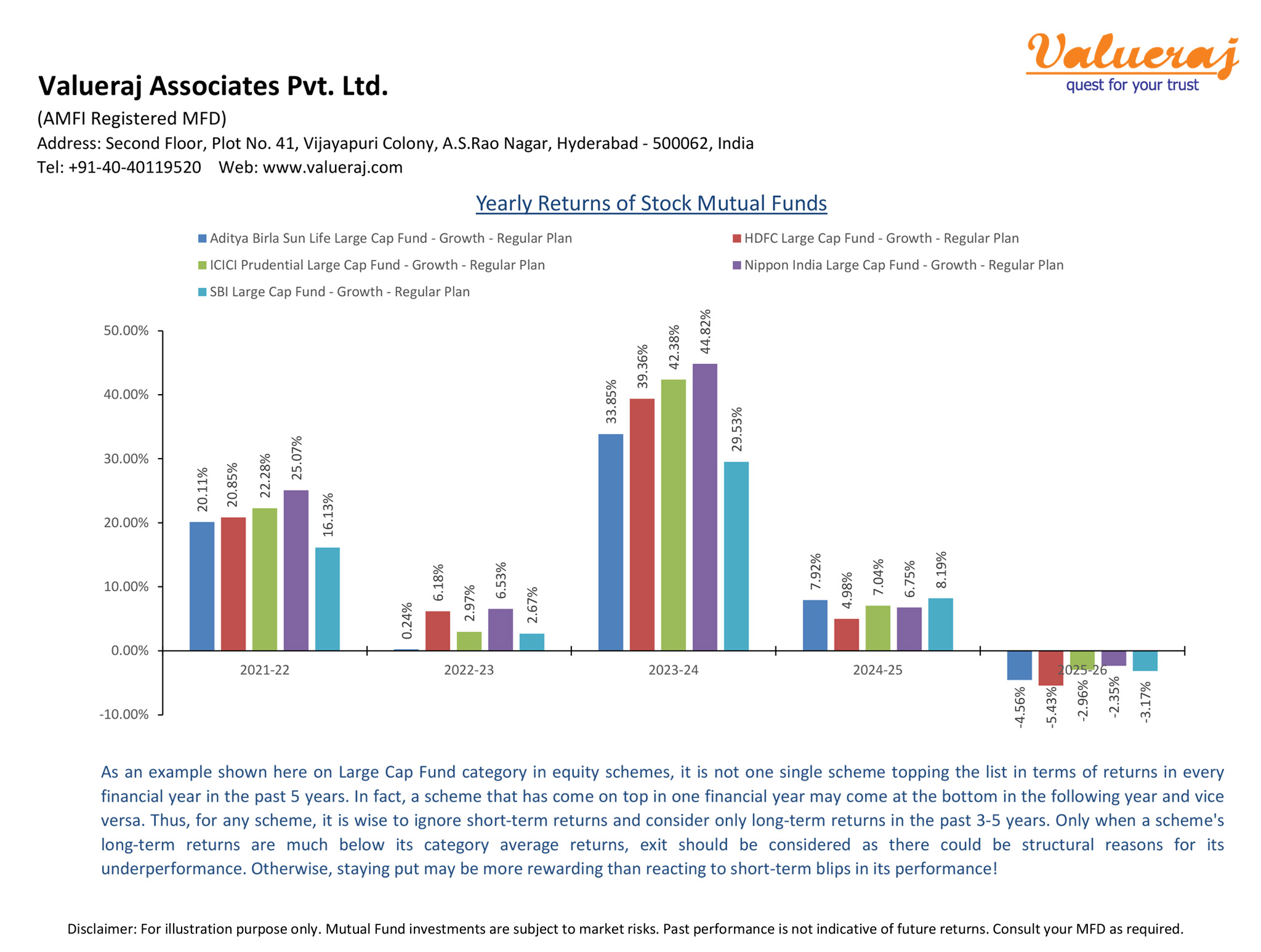

As stock markets go through ups and downs, stock mutual funds too go through volatile returns in the short-term. However, you should ignore such cyclical blips and stay invested for long-term to clinch superior returns. The reasons for any exit should be more structural rather than short-term blips. Thus comes the long-term orientation and focus on only long-term returns for investing in stock mutual funds.

For better understanding, find below our analysis on returns of some stock mutual funds in the past 5 years.

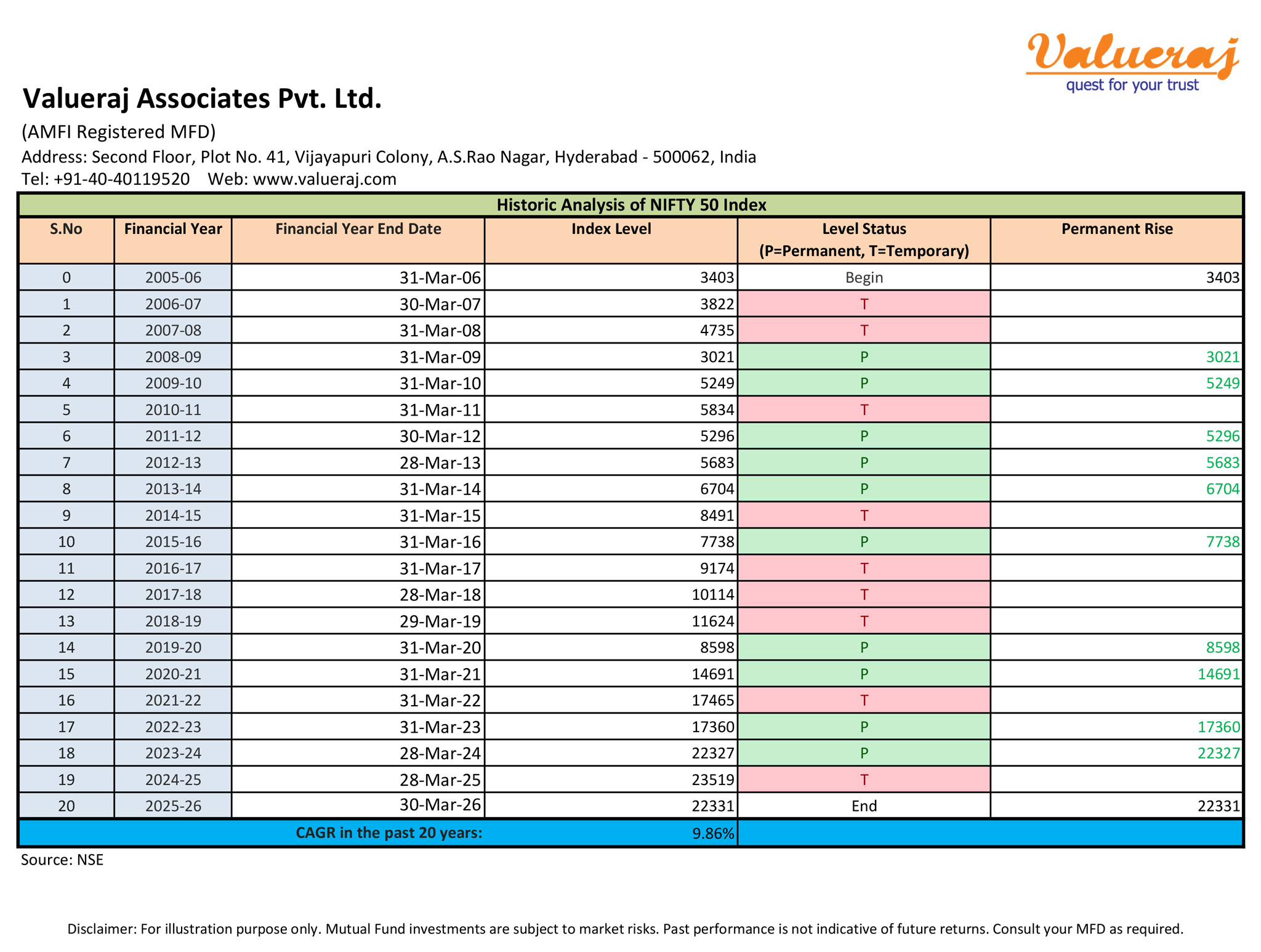

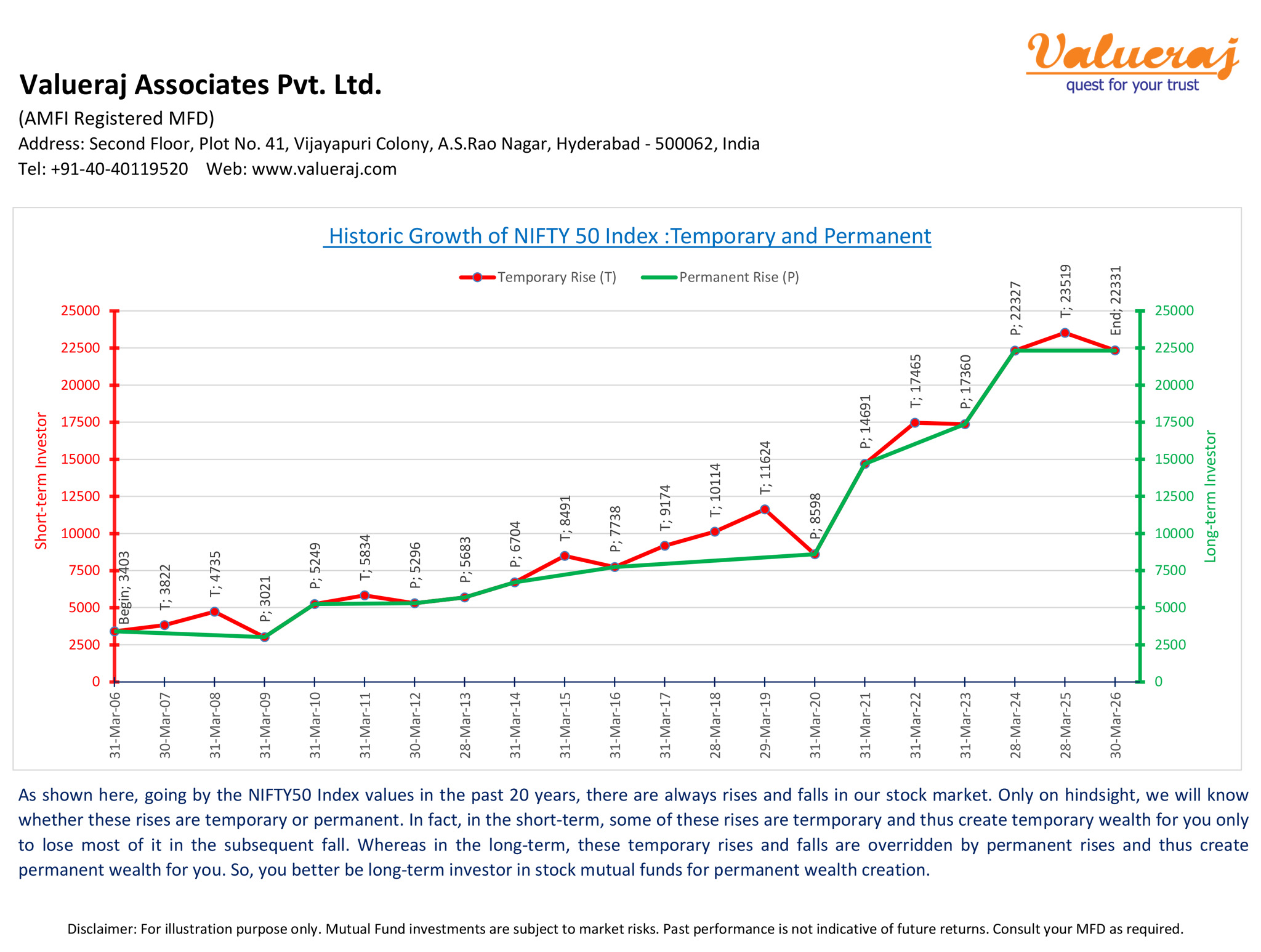

Stock markets are inherently volatile and there are always rises and falls. However, in the short-term, some of the rises create temporary wealth which will vanish in the subsequent fall. Only in the long-term, these temporary rises and falls are overridden by permanent rise and thus create permanent wealth for you.

Find below our analysis on temporary/permanent rises and falls of NIFTY50 Index in the past 20 years.

Gold as an asset class offers an excellent hedge to your investment portfolio due to its negative correlation to stock markets. Gold mutual funds can play an important role in a well-diversified portfolio with Equity/Debt/Gold funds. This asset allocation copes up with any economic uncertainty or high inflationary scenarios and thus reduces the overall volatility in the portfolio value.

For investing in Gold, find below various avenues available vis-à-vis Gold Mutual Funds.

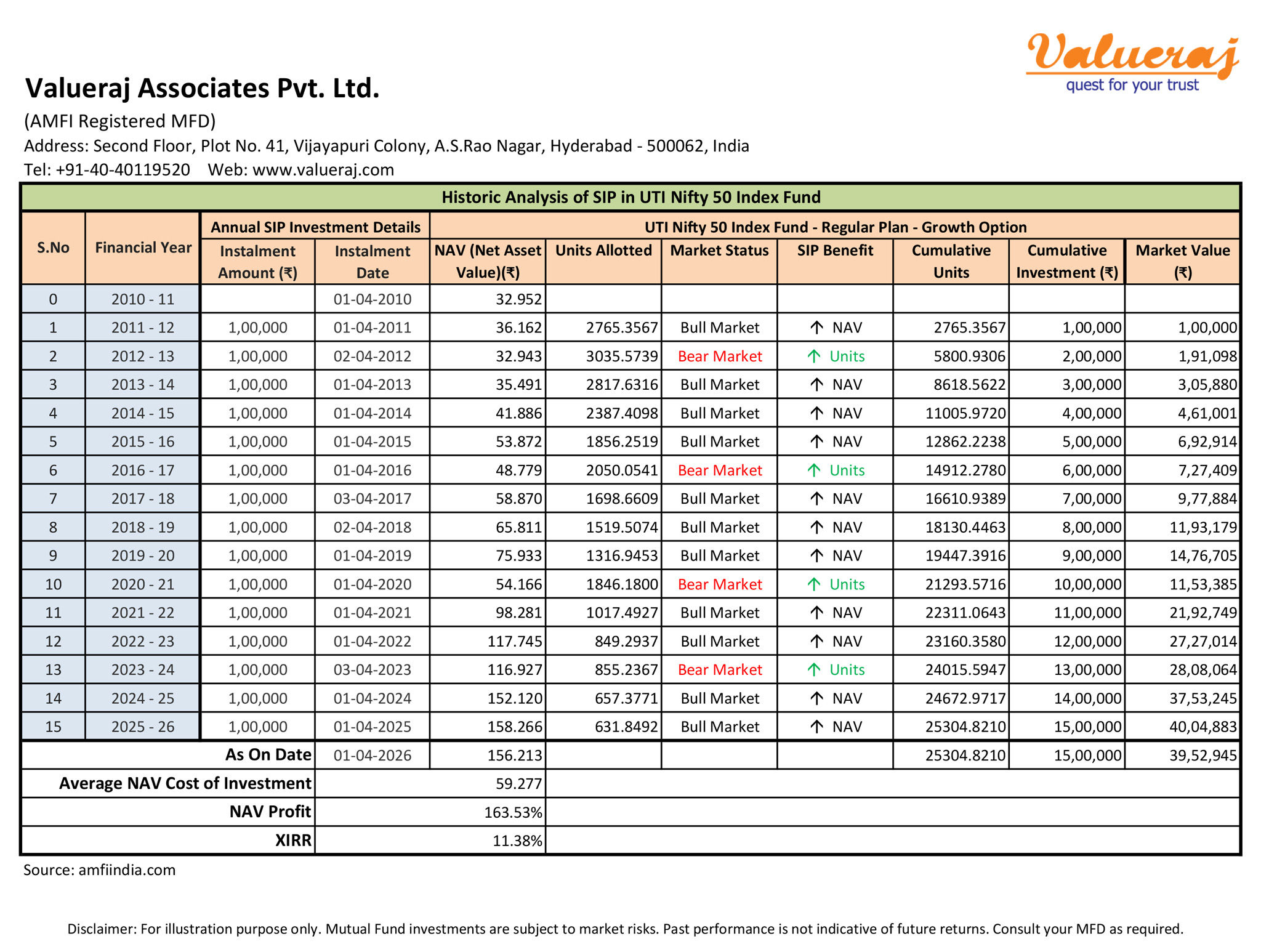

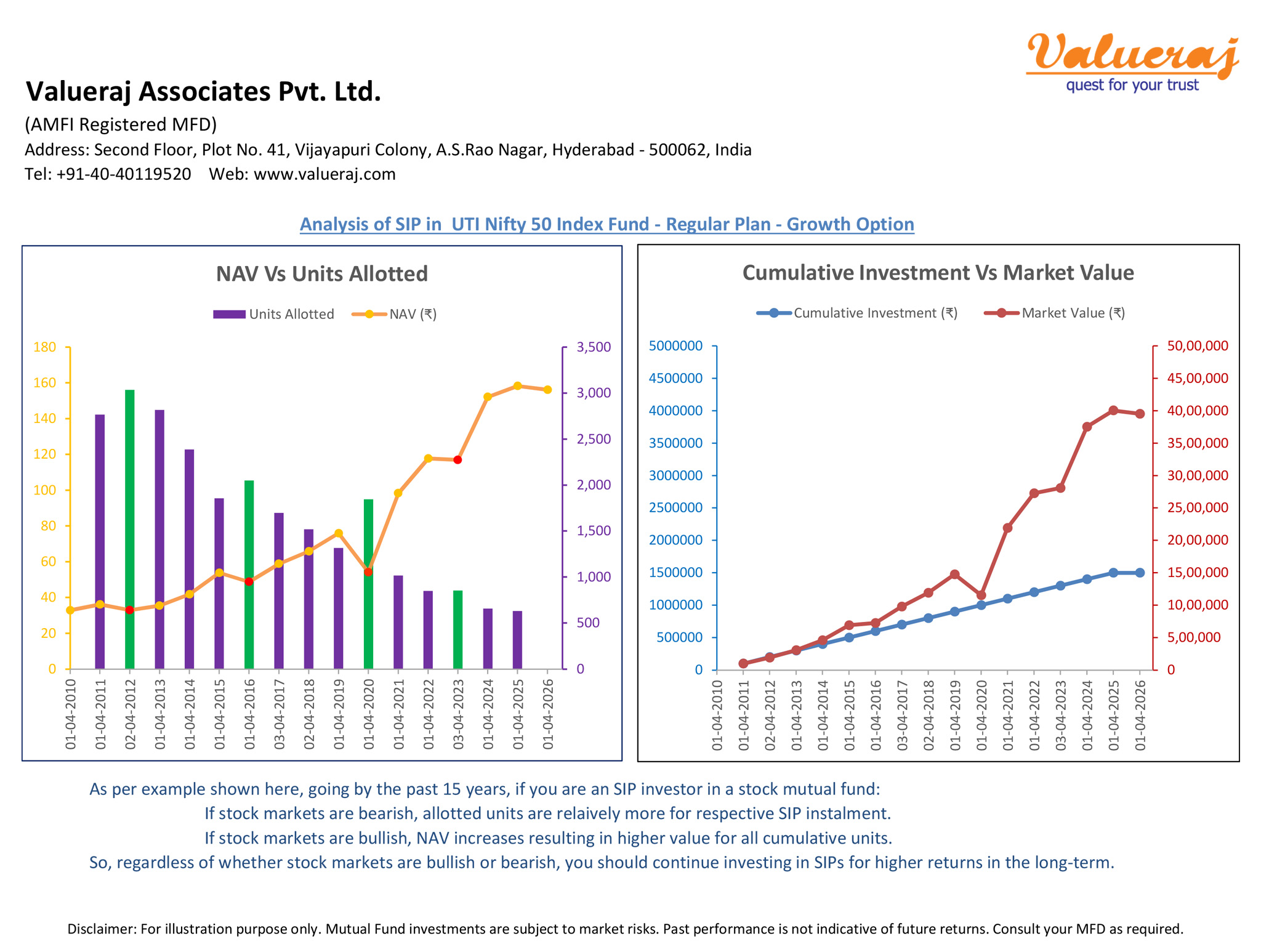

When it comes to investing in stock mutual funds, SIP (Systematic Investment Plan) method has inherent benefits. If stock markets are bearish, more units get allotted per SIP installment. If stock markets are bullish, NAV increases and so does the market value of all accumulated units. Thus, in the long-term, occasional bear markets help in reducing the average cost of investment and increasing the returns on investment.

For illustration, find below our analysis on benefits of annual SIP over last 15 years in an index fund i.e. ‘UTI Nifty 50 Index Fund – Regular Plan – Growth Option’.

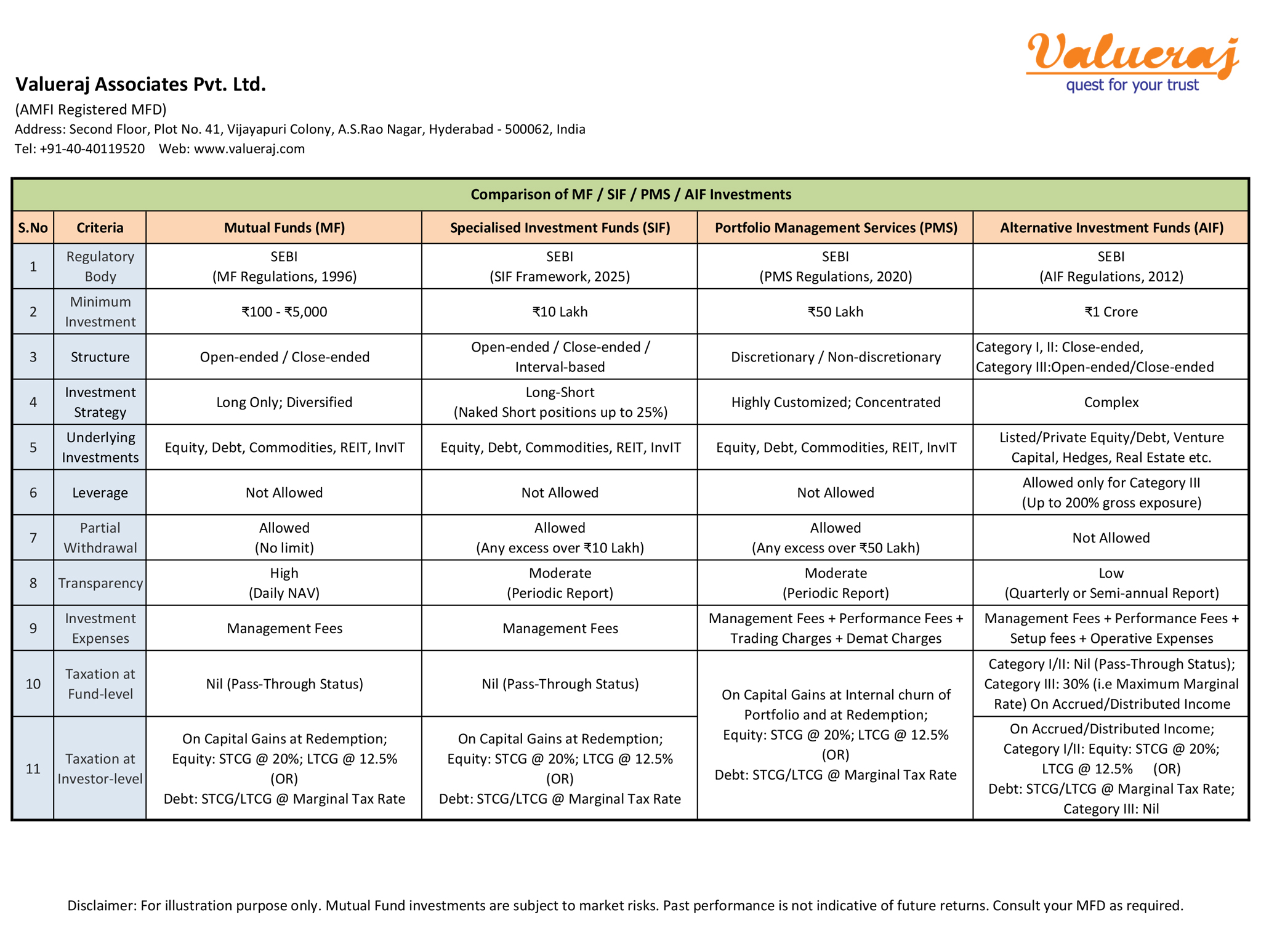

For long-term wealth creation, MF (Mutual Funds) offer the highest level of flexibility and liquidity, making them the best choice for retail investors. In contrast, Specialized Investment Funds (SIFs), Portfolio Management Services (PMS), and Alternative Investment Funds (AIFs) are tailored for High Net-Worth Individuals (HNIs), offering higher risk/return strategies but requiring higher minimum investments.

Find below detailed comparison of SIF/PMS/AIF vis-à-vis Mutual Funds.

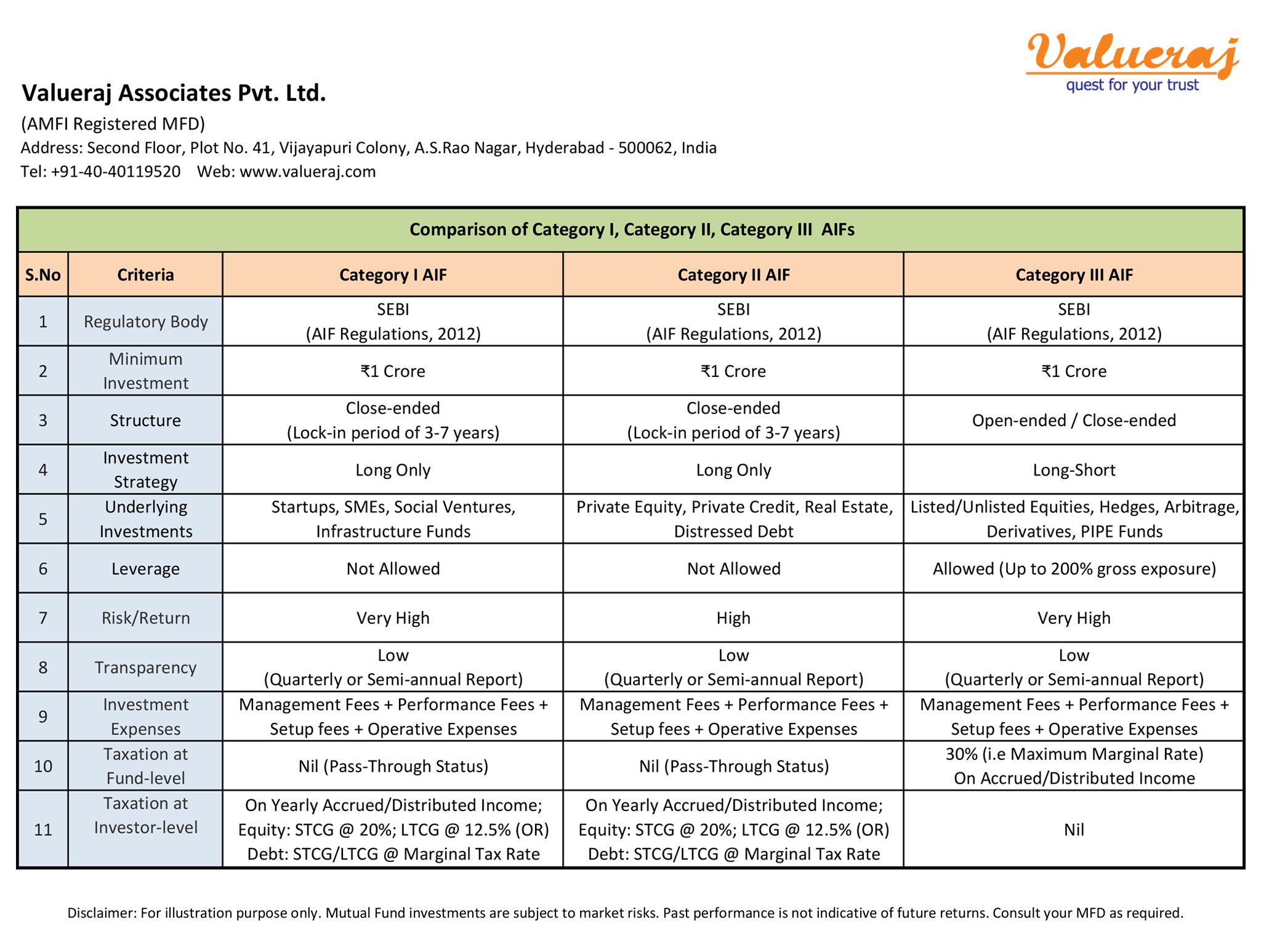

Alternative Investment Funds (AIFs) are privately pooled investment vehicles that are suitable for High Net-Worth Individuals (HNIs). AIFs invest into non-traditional asset classes like private equity, private credit, hedge funds, venture capital, real estate etc. They offer high risk/return opportunities to HNIs with long-term orientation and lower liquidity needs.

Find below a detailed comparison of various categories (Category I, Category II & Category III) in AIFs.